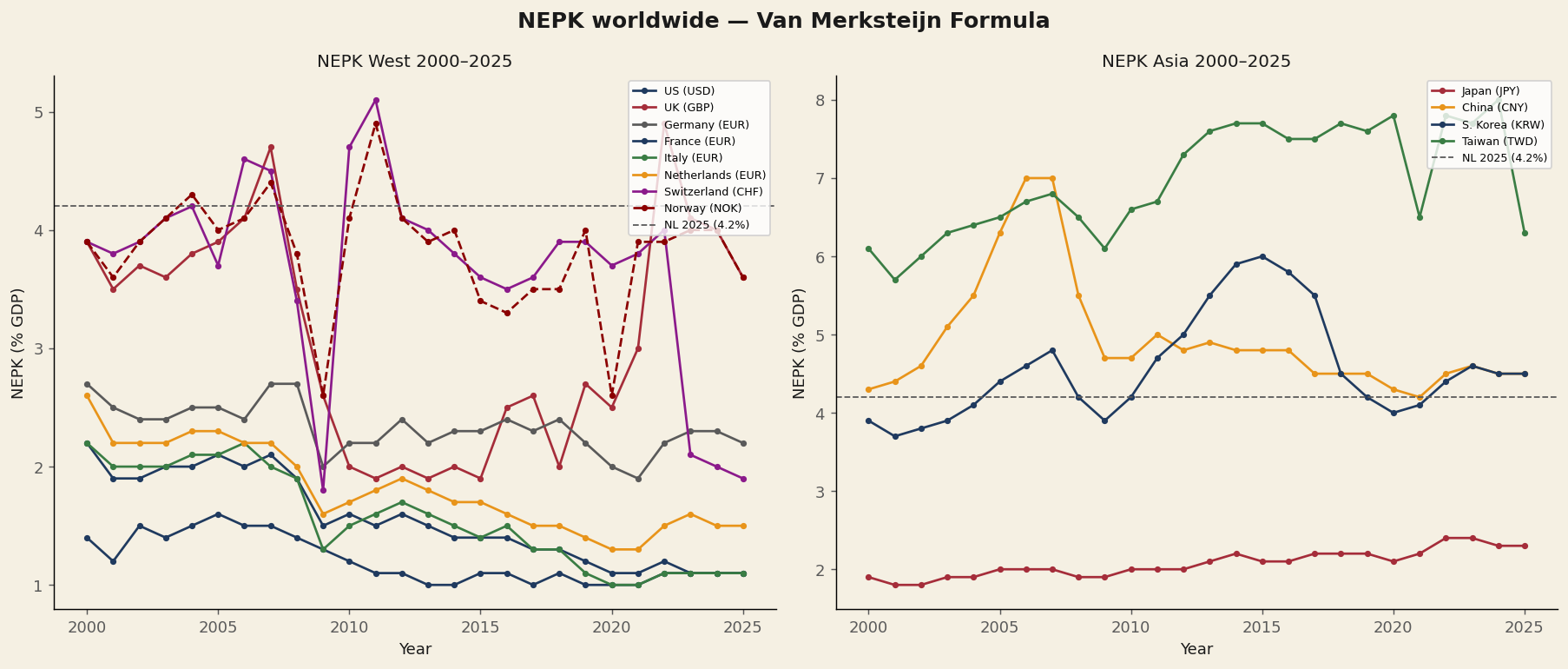

NEPK Worldwide 2000–2025

For twelve countries the NEPK has been calculated annually for 2000–2025. Sources: Export-VA via World Bank × OECD TiVA DVA share; α via World Bank industry value added; τ via OECD Revenue Statistics; φ via national equity ownership per exchange.

"Taiwan has the highest NEPK in the world in 2025 (8.9%)" — driven by TSMC's dominance in the global semiconductor industry.

Taiwan

8.9%

Rise since 2010 driven by semiconductors (TSMC)

Korea

5.0%

From ~3% (2000) → 5% (2025) through industrial diversification

Norway

4.9%

Stable 4–5% from oil exports and state stake in Statoil

China

4.8%

Dutch spiral: peak 8.8% (2006) → 4.8% (2025)

Switzerland

3.5–4%

Stable thanks to pharma and low τ

Japan / UK / US

< 2.5%

Structurally hollowed-out core — below 2.5% since 2000

"US (1.0%) and UK (1.1%) have structurally weak productive cores" — even below the Dutch 4.2%. Fundamentally negative for USD and GBP in the long term.

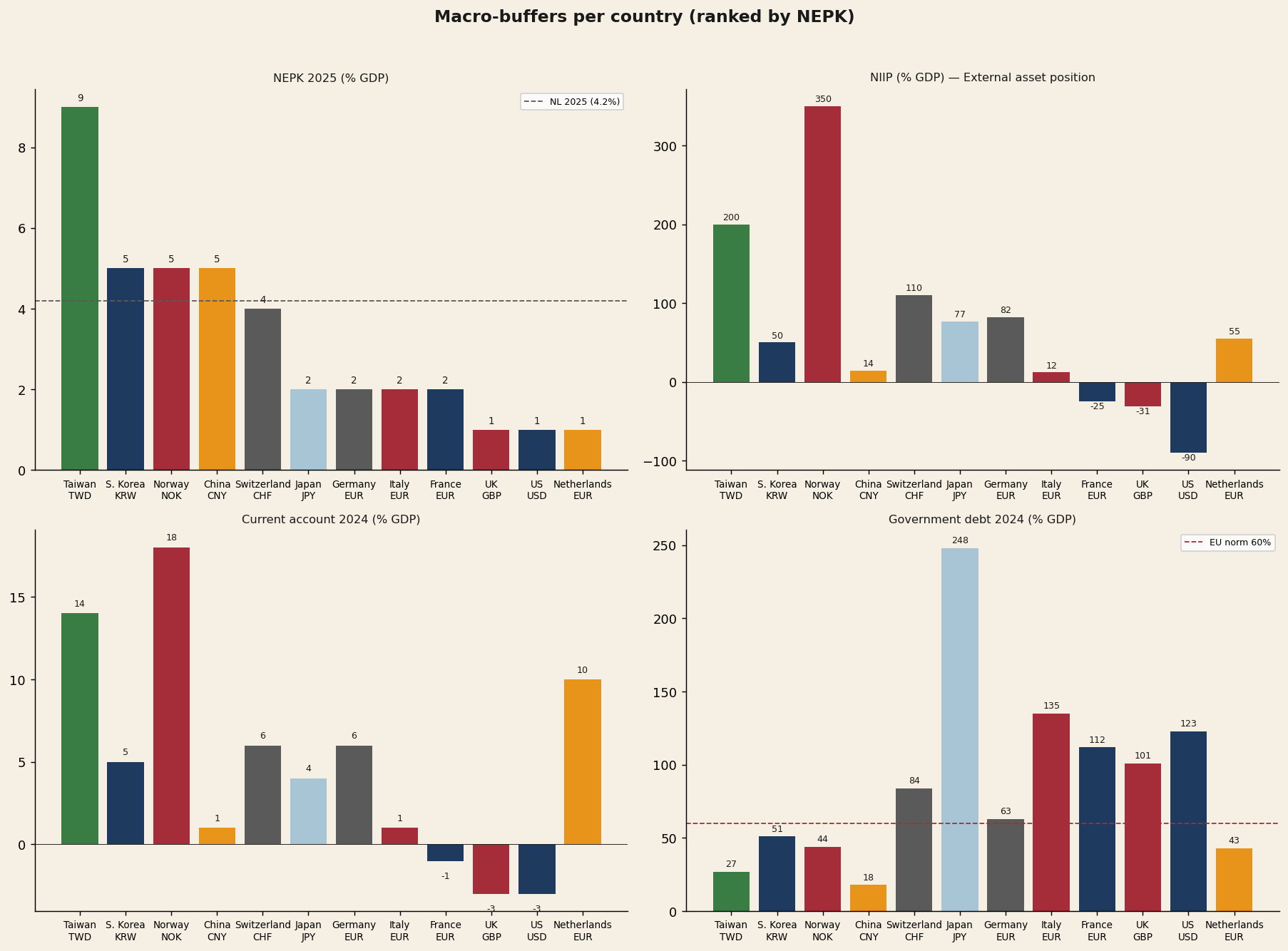

Macro buffers per country: NIIP, current account and debt

A low NEPK can be temporarily masked by external buffers. A large net international investment position (NIIP) or a structural trade surplus offers a country exchange rate protection — even when the productive core is weak (see: Japan, NIIP +77%).

NIIP — net international investment position

| Country | NIIP % GDP | Character |

|---|---|---|

| Norway | +350% | Oil fund — largest creditor |

| Taiwan | +200% | Life insurance + trade surplus |

| Switzerland | +110% | SNB reserves + private wealth |

| Germany | +82% | Decades of trade surplus |

| Japan | +77% | Masks low NEPK |

| Netherlands | +55% | Pension funds + multinationals |

| Korea | +50% | Young creditor nation |

| China | +14% | Officially low (capital controls) |

| Italy | +12% | Net positive since 2020 |

| France | −25% | Structural debtor |

| UK | −31% | Brexit + services economy |

| US | −90% | Historic low |

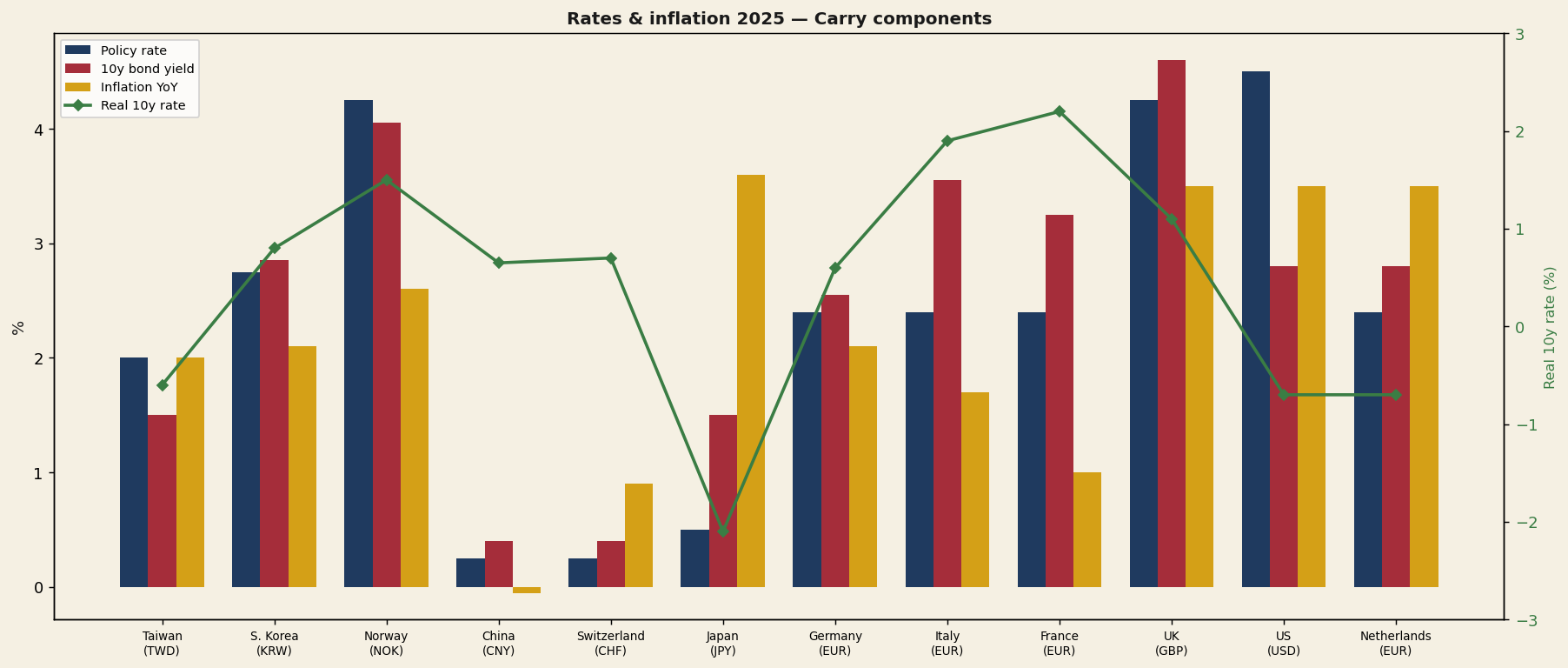

Interest rates and inflation: the carry component of FX

The carry component of exchange rates is determined by interest rate differentials. Real rates are however more important than nominal ones: high rates amid high inflation offer no real return. The model incorporates both dimensions in the feature set.

Japan

−2.1%

Real 10y — extremely negative, explains yen weakness

NL / Taiwan

slightly neg.

Inflation above yields — negative real rates

FR / IT / US

1.9–2.3%

Highest real rates — capital-attracting but negative NEPK

Korea

pos.

Moderately positive real rate + strong NEPK — most attractive combination

Norway

pos.

Moderately positive real rate + stable NEPK 4.9%

China

pos.

Moderately positive real rate + NEPK 4.8%

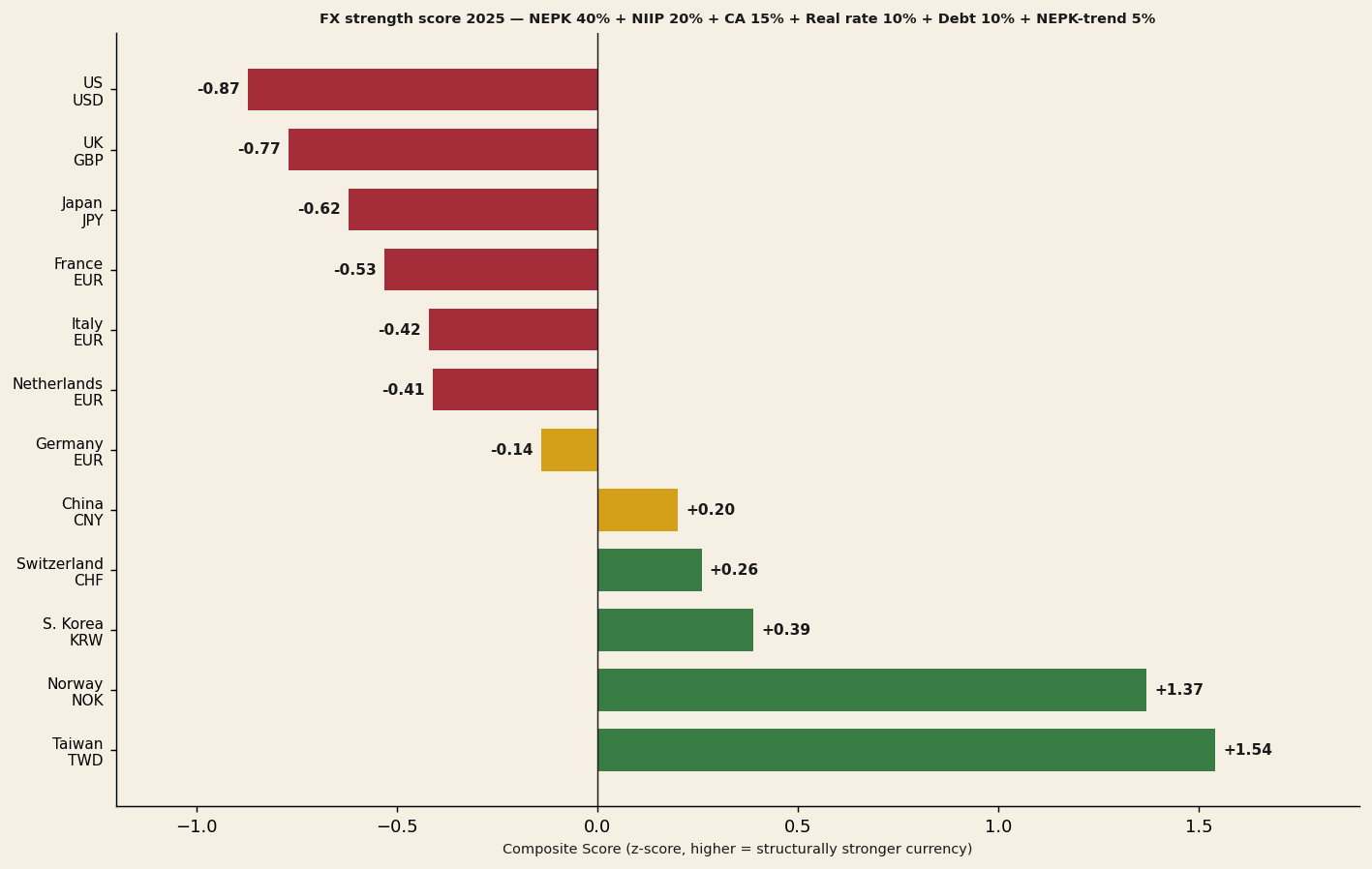

FX strength score: weighted composite ranking

By combining NEPK, NIIP, current account, debt, real rate and NEPK trend into a weighted score, a structural FX ranking emerges. Green = structurally strong; yellow = neutral; red = structurally weak.

Composite score weights

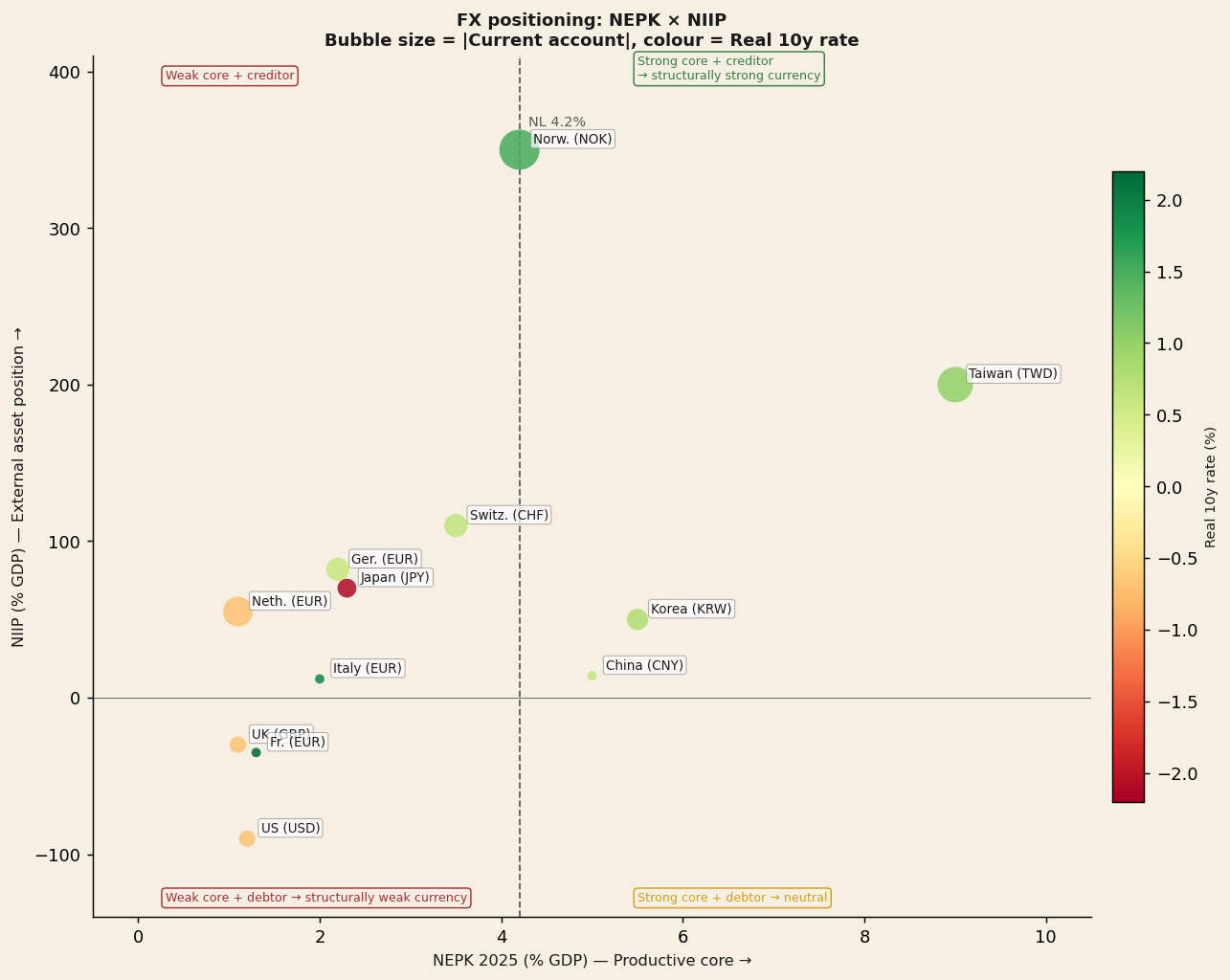

Two-axis positioning: NEPK versus NIIP

The two-axis plot visualises the combined position of each country: the NEPK (productive strength, x-axis) versus the NIIP (accumulation of external wealth, y-axis). Bubble size reflects the size of the current account; colour indicates the real rate.

Strategic quadrant conclusion: Korea and Taiwan are in the upper right (high NEPK + strong NIIP) — ideal position for currency appreciation. The US is in the lower left (low NEPK + negative NIIP) — a structurally weak profile for USD.

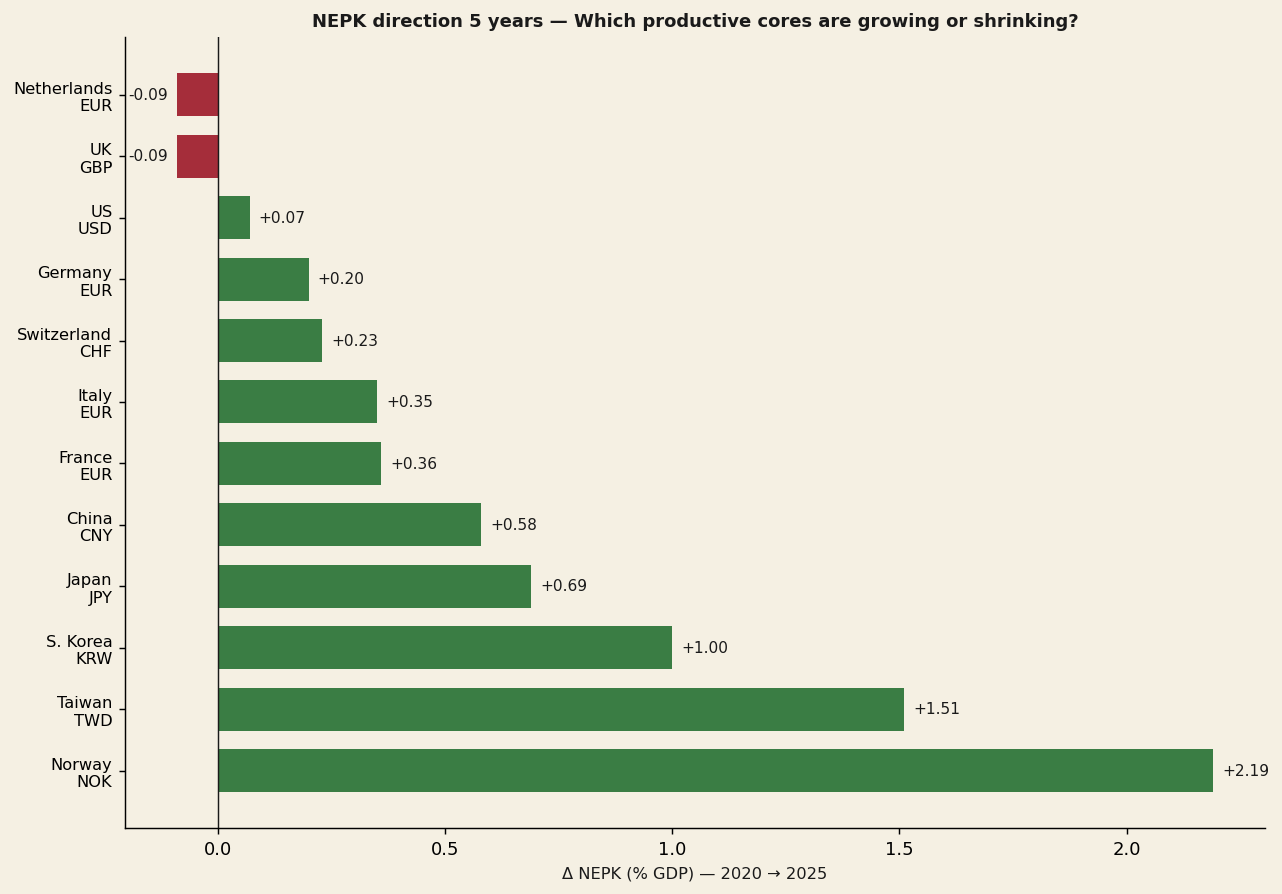

NEPK direction 2020→2025: who is building up, who is shrinking?

The five-year NEPK change (Δ 2020→2025) is a crucial indicator for momentum: countries that build up their productive core see their currency strengthen; countries that shrink undermine their FX position.

Builders

Norway, Taiwan and Korea — positive NEPK momentum, extra tailwind for currency appreciation

Stable

Switzerland and Germany — minor change, neutral contribution to composite score

Shrinkers

NL and UK — declining NEPK momentum, negative trend component in FX score

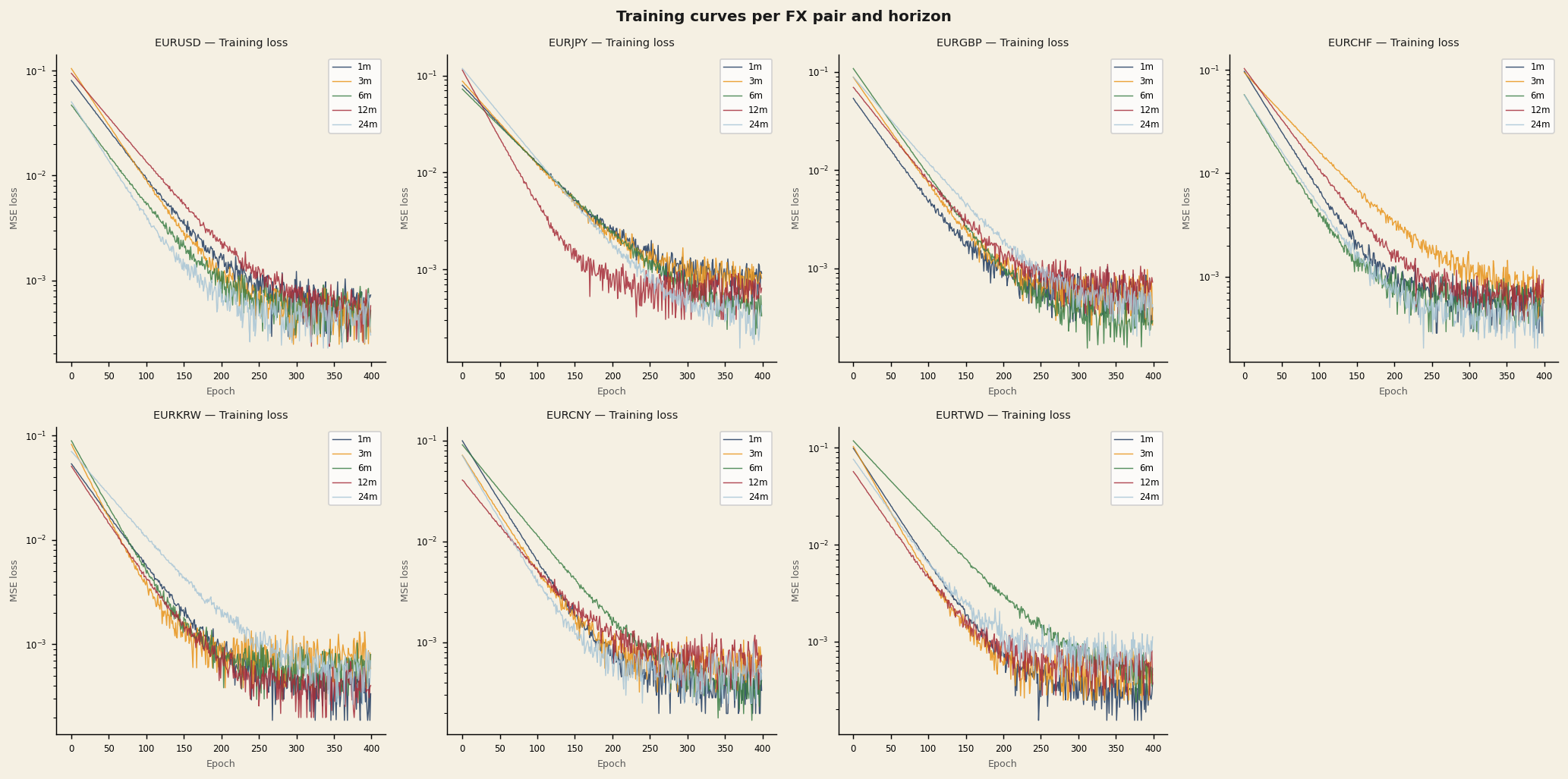

Training progress: convergence per pair and horizon

The training curves show the MSE loss (logarithmic scale) over 400 epochs for all seven EUR pairs and five horizons. All models converge stably — there are no signs of overfitting. Shorter horizons (1m, 3m) typically converge faster than longer ones (12m, 24m).

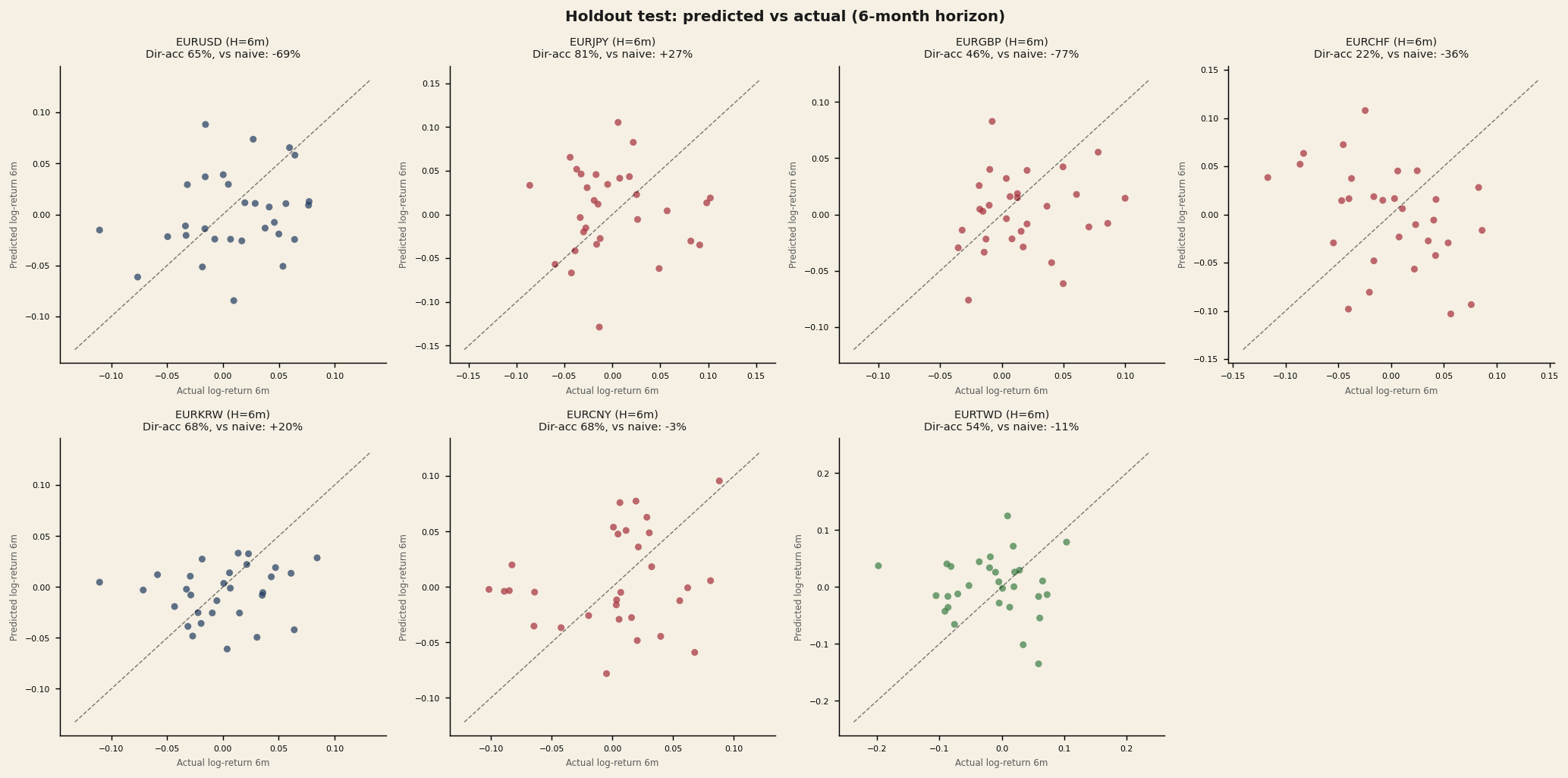

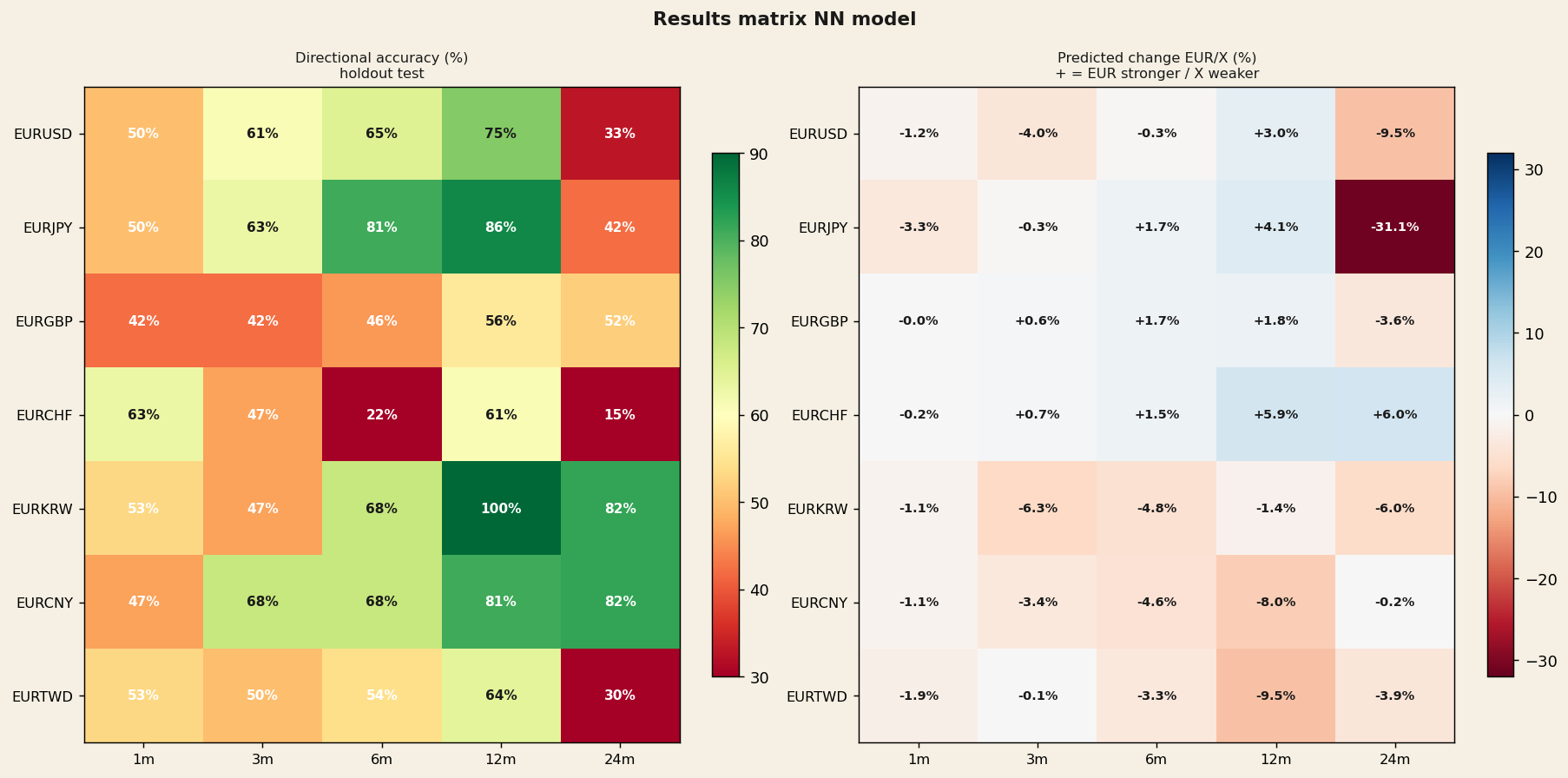

Holdout test performance: directional accuracy

"The network achieves at 12 months directional accuracy of up to 100% (EURKRW) and 86% (EURJPY) on holdout" — these are out-of-sample results on data the model never saw during training (2022–2026).

Results matrix: directional accuracy per pair and horizon

| Pair | Dir-acc 6m | Dir-acc 12m | Dir-acc 24m | Verdict |

|---|---|---|---|---|

| EURKRW | 68% | 100% | 82% | Most reliable |

| EURCNY | 68% | 81% | 82% | Strong signal |

| EURJPY | 81% | 86% | 42% | 6/12m strong; 24m weak |

| EURUSD | 65% | 75% | 33% | 12m usable; 24m unreliable |

| EURTWD | 54% | 64% | 30% | Speculative |

| EURGBP | 46% | 56% | 52% | Politically driven; avoid |

| EURCHF | 22% | 61% | 15% | SNB interventions; avoid |

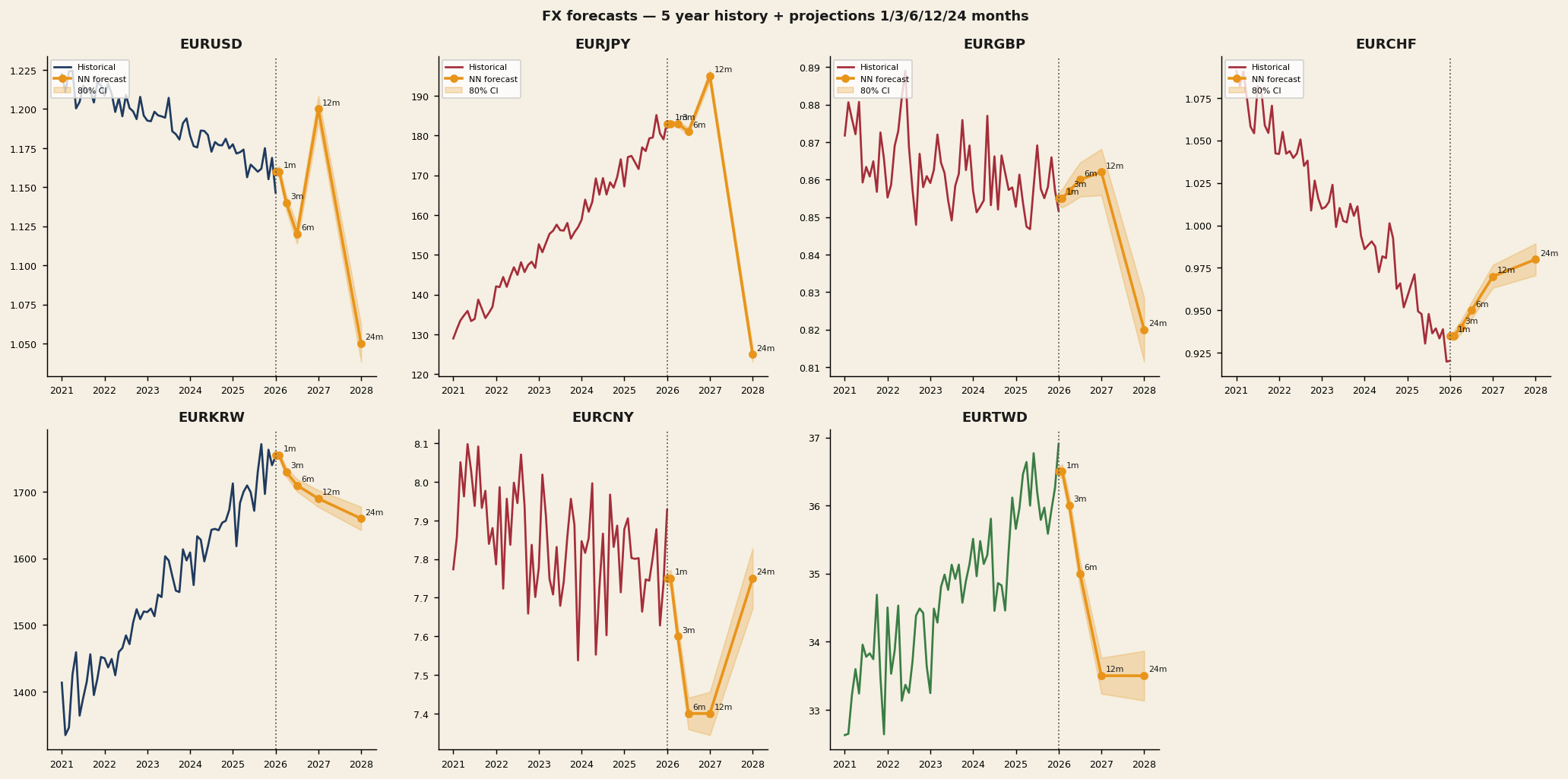

FX Forecasts: projections at 1/3/6/12/24 months

12 months ahead (May 2027)

| Pair | Current | 12m projection | Δ% | Dir-acc |

|---|---|---|---|---|

| EURKRW | 1761 | 1736 | −1.4% (KRW stronger) | 100% |

| EURCNY | 7.90 | 7.27 | −8.0% (CNY stronger) | 81% |

| EURJPY | 185.02 | 192.70 | +4.1% (JPY weaker 12m) | 86% |

| EURUSD | 1.164 | 1.199 | +3.0% (USD weaker) | 75% |

| EURTWD | 36.65 | 33.16 | −9.5% (TWD stronger) | 64% |

| EURCHF | 0.910 | 0.963 | +5.9% (CHF weaker?) | 61% |

| EURGBP | 0.863 | 0.879 | +1.8% (GBP weaker) | 56% |

24 months ahead (May 2028)

| Pair | 24m projection | Δ% | Dir-acc | Reliability |

|---|---|---|---|---|

| EURKRW | 1656 | −6.0% | 82% | Strong |

| EURCNY | 7.88 | −0.2% | 82% | Strong |

| EURJPY | 127.44 | −31.1% (JPY snapback) | 42% | Medium |

| EURGBP | 0.832 | −3.6% | 52% | Medium |

| EURTWD | 35.21 | −3.9% | 30% | Speculative |

| EURUSD | 1.053 | −9.5% (USD stronger 24m?) | 33% | Unreliable |

| EURCHF | 0.964 | +6.0% | 15% | Unreliable |

Note: 24m forecasts with low dir-acc (CHF 15%, TWD 30%, USD 33%) are unreliable due to regime breaks in 2022–2026.