The original Brussels Consequences Map showed the price of Brussels' current climate and industrial policy: a net loss of between five and fifteen per cent for the average European citizen or business by 2030. It was a map of damage.

This piece shows what happens when Brussels no longer chooses damage. When the Green Deal and CBAM — the two most costly mechanisms — are replaced by a single instrument: BiCRS (a product of Carbon-Alert Ltd) via anoxic biomass injection, produced entirely within the equatorial band, at forty euros per tonne of CO₂. The same climate objective, a fundamentally different outcome.

The question is no longer: how much damage does the European prosperity base suffer because of Brussels? The question becomes: how much gain does Europe generate through Brussels? The answer, in modelling terms, is a net effect of plus 23 to plus 106 per cent per scenario by 2030. Not because climate policy has been abandoned, but because climate policy has been redesigned — and because production is sited where the plant grows, not where the accountant sits.

What BiCRS-via-anoxic-biomass-injection is

BiCRS stands for Biomass Carbon Removal and Storage. In the variant this piece models, the mechanism is strikingly simple: tropical biomass is grown and harvested on equatorial land. The harvested biomass is then liquefied on the field itself, through a special cell-wall-disrupting process — the intracellular water is released so that the plant mass turns into a thick, pumpable liquid. This liquid is introduced underground directly on site, right beneath the roots of the crop that produced it, through injection tubing at a depth of 1.2 to 1.4 metres.

There is no transport. No lorry, no tanker, no storage shed, no logistics chain between harvest and storage. The biomass liquid is injected into the same soil column from which it grew — beneath the same roots that will produce it again next season. This makes the operation a closed loop at the hectare level: plant, harvest, liquefy, inject, plant again. Not a single molecule of carbon leaves the plot.

At that depth there is no oxygen present. Without oxygen, bacterial oxidation of plant material is not possible. The result is that the injected biomass liquid undergoes a process resembling natural peat formation, but accelerated and with homogeneous distribution: between 90 and 95 per cent of the plant carbon remains permanently — for hundreds of years — locked into the soil beneath the plantation.

This is not BECCS — nothing is burnt, there is no capture installation, no flue gas stream. This is not biochar — no pyrolysis, no heat input. Nor is it gas or CO₂ storage under pressure in distant geological formations. It is a fundamentally simpler mechanism: liquefied biomass is dispersed underground in situ, beneath the plant's own root zone, after which anoxic peat formation locks the carbon away permanently.

The economic key is precisely that simplicity. No energy plant is needed, no carbon-capture installation, no pipeline network, no geological reservoir survey, no transport fleet. Only growing biomass, liquefying it on the field through the special cell-disruption process, and injecting it on site at a depth reachable with standard agricultural equipment. The liquid state is what makes the system scalable: liquids can be pumped, dosed and evenly distributed in a way that solid biomass does not allow — and the in-situ operation is what makes it cost-competitive, because the logistics layer falls away entirely.

Where BiCRS is possible — and why only there

A fundamental fact that guides this piece: the plant which delivers the yields that make BiCRS economically viable grows exclusively in the equatorial climate zone. Three conditions are cumulatively necessary:

• Sufficient sunlight — year-round, without seasonal variation

• Sufficient water — regular rainfall or available irrigation

• Temperature above 6 degrees Celsius — below this threshold the plant dies

This means that production within Europe simply does not pay. Not in southern Spain, not in Sicily, not in Romania. European alternatives such as Miscanthus achieve at most one hundred to one hundred and ten tonnes of CO₂ per hectare at fifty to sixty euros per tonne — half the tropical yield at a fifty per cent higher price. The comparison has been worked through and points unambiguously: one hundred per cent equatorial production is superior both economically and in climate terms.

Production lies within the equatorial band between 10 degrees north and 10 degrees south — an area of roughly 5 billion hectares. Europe's role thereby changes fundamentally: from producer to investor, buyer and contracting partner. This is not a handicap — it is a strategic opportunity. It turns the BiCRS system into a renewed European-African-Asian economic axis, comparable to how the solar-energy revolution defined the Chinese-European axis in the 2010s.

The calculation — 200 tonnes of CO₂ per hectare per year

The calculation below follows the fixed plant-physiological ratios and is verifiable against any scientific standard.

Fresh biomass per hectare per year: 400 tonnes

× dry-matter fraction (22-25%, avg 23.5%): 94.0 t dry matter/ha

× carbon fraction (46-48%, avg 47%): 44.2 t C/ha (total in plant)

× retention under anoxic conditions (92.5%) 40.9 t C stored/ha

× molecular ratio CO₂/C (3.666): 150 t CO₂/ha (above ground)

+ root mass permanently in soil (25%): 50 t CO₂/ha (below ground)

Total per hectare per year: 200 t CO₂/ha

One hundred and fifty tonnes of CO₂ per hectare are actively stored via biomass injection. Fifty tonnes come automatically from the root mass that remains in the soil after harvest, between zero and two metres deep — a natural form of storage that requires no further intervention. Together they yield two hundred tonnes per hectare per year.

Scale — what the world and Europe need

Multiply this figure by global and European implementation and the order of magnitude becomes visible:

Global CO₂ emissions 2024: 37 Gt CO₂/year

Hectares needed for global net zero: 185 million hectares

as % of world land surface: 1.25%

as % of equatorial band: 3.7%

Hectares needed for EU net zero: 14 million hectares

for comparison — Greece: 13.2 Mha

as % of EU farmland affected: 0% — none

For European net zero: fourteen million hectares of equatorial production. An area slightly larger than Greece — but distributed across six to eight supplier countries to avoid geopolitical dependence on any single one. Crucially: zero per cent of European farmland is affected. No food conflict, no land claim within Europe, no competition with European arable farming. Europe buys in the capacity where it can be supplied — the equatorial band — and pays a transparent price of forty euros per tonne of CO₂ for it.

Strategic partner arrangements — the European-equatorial alliance

One hundred per cent equatorial production means that the entire European BiCRS rollout rests on contracts with partner countries. That sounds like a vulnerability; in reality it is the strength of the model. A two-sided interest — Europe gains climate security, the partner countries gain long-term high-value export income — creates the most stable conceivable basis for long-term cooperation. This is not development aid, and not a colonial extraction model. It is a structured commercial alliance with an explicit development component.

Six to eight partner countries — the portfolio

The Brussels offer concerns fourteen million hectares of biomass production. No single country supplies more than twenty per cent of the total — a hard diversification limit, a lesson drawn from the Russian gas crisis of 2022. The proposed distribution:

Congo-Kinshasa + Congo-Brazzaville: 2.8 Mha (20%)

Brazil (Amazon edge, degraded): 2.8 Mha (20%)

Indonesia (Sumatra, Kalimantan): 2.1 Mha (15%)

Nigeria (Middle Belt): 1.4 Mha (10%)

Ghana + Ivory Coast: 1.4 Mha (10%)

Malaysia (Sabah, Sarawak): 1.4 Mha (10%)

Philippines + south India + other: 2.1 Mha (15%)

Total portfolio: 14.0 Mha (100%)

Each of these countries has available degraded farmland — former oil-palm plantations, exhausted cocoa fields, abandoned savannah arable land — that can be deployed without rainforest conversion. Africa alone has, according to FAO estimates, around 400 million hectares of degraded farmland. The portfolio touches less than four per cent of that reserve.

The contract model — hybrid state-and-business

The contracts are hybrid. Brussels negotiates the framework treaty with the partner country — duration, price floor, development component, monitoring protocol. Within that framework, private operators (European biomass companies, local joint ventures) carry out production. This combines the advantage of state security with the efficiency of commercial operation.

Four core elements per framework treaty:

One — duration of fifteen to twenty-five years. Anything shorter does not work: BiCRS requires two to three years of ground preparation before the first harvest. No supplier will make the investment without certainty of offtake over the lifetime of the plantation. A twenty-five-year contract at forty euros per tonne provides that certainty — and ties the partner country into a trajectory that structurally connects it to the European economy.

Two — a guaranteed minimum price in euros, indexed for inflation. Forty euros per tonne of CO₂ is the starting point; if the European ETS reference price rises, the supplier shares in a fixed percentage of the surplus. If the ETS price falls, the floor of forty euros remains intact. This prevents the cyclical price swings that have made palm oil, cocoa and coffee such vulnerable export products.

Three — a mandatory development component. Ten per cent of the European payment does not go to the operator, but to a local development fund with mixed governance — partner-country government, supplier community, European representation. This fund builds schools, clinics, agricultural-extension services and roads. It makes the BiCRS contract politically acceptable within the partner country — and legally defensible against Western non-governmental organisation criticism.

Four — strict exclusion of primary rainforest. Independent satellite monitoring via Copernicus and Planet Labs. Upon a confirmed breach: a contract penalty plus a temporary offtake suspension. This is not a watertight guarantee — no control ever is — but it is the highest conceivable level of due diligence achievable with current technology. Production exclusively on degraded farmland, savannah areas and disused industrial zones.

What the supplier countries receive — the figures

For a Congolese farmer who converts one hectare from cassava (current source of income: around €300 per hectare per year) to BiCRS biomass under contract: two hundred tonnes of CO₂ × forty euros = eight thousand euros gross. After operator margins, depreciation of injection equipment and operating costs, he keeps an estimated two to three thousand euros net. That is seven to ten times his current income — a transformative shift for the rural Congolese household. Because the injection takes place on his own plot, he does not have to transport any biomass — the mobile cell-disruption and injection equipment comes to him, not the other way round.

At country level: Congo-Kinshasa, with 2.8 million hectares under BiCRS contract, receives annually 2.8 Mha × 200 t × €40 = 22.4 billion euros gross. That is about twenty per cent of current Congolese GDP — an inflow on a scale comparable to the petroleum exports of Nigeria or Angola, but via a renewable and geographically dispersed source. For Indonesia, with 2.1 Mha, this comes to 16.8 billion euros per year; for Brazil, to 22.4 billion for the Amazon-edge component.

This is not charity. It is a commercial relationship in which the partner country supplies where it has a comparative advantage (climate, sunlight, water) and Europe pays where it has a comparative need (climate policy, industrial competitiveness, energy independence). It is precisely the kind of connection that the decolonisation of the 1960s never managed to deliver — a durable North-South economic bond without debt bondage or structural-adjustment package.

Political route — Brussels ratification partnership by partnership

In practice, three or four vanguard contracts begin in 2027-2028 with the most stable and best-governed partner countries — for example Ghana, Ivory Coast, Brazil (the states of Pará and Tocantins, with strong governors), and Indonesia (the provinces of North Sumatra and South Kalimantan). These anchor contracts serve as a pilot format for the remaining partner countries. Subsequently, Congo-Kinshasa, Congo-Brazzaville, Nigeria, Malaysia and the Philippines are added in the second wave (2028-2029).

Brussels ratification proceeds per framework treaty via a Council decision by qualified majority, after the opinion of the European Parliament. Not via an association agreement requiring unanimity — that is procedurally unnecessary and would make the system politically blockable by a single dissenting member state. BiCRS contracts are commercial offtake commitments under the Union's climate and trade competence, not political alliance treaties.

Bioethanol as a separate second track

Alongside BiCRS there is a second equatorial biomass application: bioethanol production. It is crucial to stress that these are two fundamentally different tracks, entirely independent of one another. They are not two products from the same harvest. A hectare is either a BiCRS hectare or an ethanol hectare. The biomass, the operations, the infrastructure and the value chain differ for the two tracks.

Two separate routes

BiCRS route. Mobile cell-disruption and injection equipment comes to the plot. The biomass is liquefied on site and injected right beneath its own roots. No transport, no factory, no logistics chain. The carbon stays permanently in the soil beneath the crop. This is an in-situ economy.

Ethanol route. The harvested biomass is transported by lorry from the plantation to a large fermentation and distillation plant. That plant stands locally within the equatorial production region — typically within fifty to one hundred kilometres of the cultivation fields, comparable to the logistics of a Brazilian sugarcane plant. In the plant the biomass is processed into bioethanol. The ethanol leaves the equatorial production country by tanker towards European ports. This is a factory economy.

The choice between the two routes is made region by region on the basis of soil quality, water access, distance to ports, existing processing infrastructure and the investment climate in the partner country. A BiCRS cluster consists of dispersed plantations with mobile injection equipment that travels from plot to plot during the harvest season. An ethanol cluster consists of an industrial plant with a ring of supply plantations around it — typically ten to fifteen thousand hectares per plant.

The climate difference between the two tracks

BiCRS removes carbon permanently from the atmosphere. The plant captures CO₂ during growth; the injection locks that carbon away in the soil for hundreds of years. Net result: less CO₂ in the atmosphere than before the cycle. This is the mechanism on which the net-zero objective of the Brussels model rests.

The ethanol track is more climate-neutral. The plant captures CO₂ during growth, and the combustion of the ethanol in European engines releases that CO₂ again. It is a closed short-term carbon cycle, comparable to a wood-stove economy but scaled industrially. The climate gain comes from replacing fossil fuel — not from removing existing atmospheric carbon. Only BiCRS does the latter.

The Brussels portfolio choice in this piece: the entire equatorial BiCRS portfolio of fourteen million hectares is destined for in-situ injection. Bioethanol production proceeds via additional, non-overlapping hectares in the same partner countries, with its own plant infrastructure and its own contract model. The figures for the Brussels Consequences Map BiCRS version deal with the BiCRS track; the ethanol track is a complementary value chain on top of it.

Costs — €40 per tonne in the Brussels model

The proposed model price is forty euros per tonne of CO₂ — well above the actual production cost of twenty-two to twenty-eight euros, but below the current European ETS price of around seventy-eight euros per tonne. Forty euros gives Brussels room for a build-up margin, project reserve, contract administration, monitoring systems and governance costs without undoing the fundamental competitive breakthrough. The transport-and-storage chain is not in this margin — for the simple reason that it does not exist, because the CO₂ never leaves the plot.

BiCRS model price (Brussels assumption): €40/t CO₂

Comparison: current EU ETS price 2026: €78/t CO₂

Comparison: CBAM implementation 2026: €82/t CO₂

Actual BiCRS in-situ production cost: €22-28/t

of which transport and logistics: €0 — in-situ

Cost of European net zero per year: €112 bn (0.7% EU GDP)

Cost of global net zero per year: €1.48 trn (~1.5% world GDP)

For comparison: the annual cost of the current European Green Deal implementation is estimated by DG CLIMA at four to six per cent of EU GDP once all Fit-for-55 targets are met. BiCRS injection at forty euros per tonne delivers the same climate result — net zero — at about a sixth of that cost. Moreover, that expenditure does not flow into domestic compliance administration, but into a productive connection with the equatorial band. And because the injection takes place in situ — beneath the crop's own roots — the entire transport layer that normally makes up thirty to fifty per cent of carbon-capture project costs falls away.

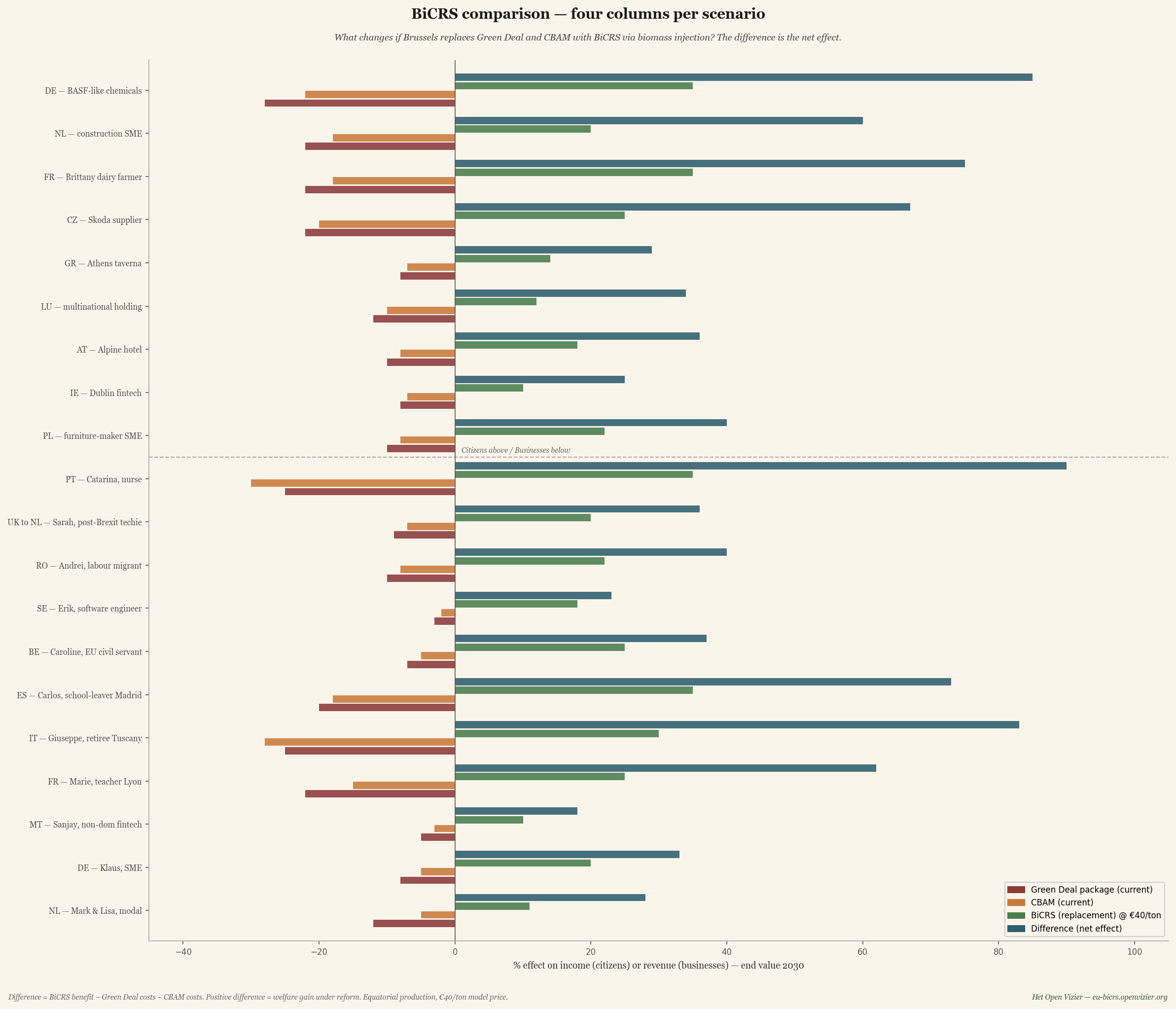

The comparison — four columns per scenario

Before the large matrix comes a first compact comparison: four columns per scenario that visualise the complete reform. First the two damage columns from current policy (Green Deal and CBAM), then the BiCRS replacement, and finally the net difference — what the net effect of the reform is.

Comparison chart — four columns per scenario: Green Deal (current loss), CBAM (current loss), BiCRS replacement (new benefit), and the net difference. The dark-blue difference column is consistently positive.

The difference figure is calculated as: BiCRS benefit minus Green Deal cost minus CBAM cost. When the Green Deal and CBAM have negative effects, the difference becomes doubly positive — the BiCRS benefit registers in full the moment the old costs fall away.

Three observations from this four-column chart.

One — Catarina (a Portuguese nurse) and Giuseppe (an Italian pensioner) receive the largest difference: well above 100 per cent of their income. This is no exaggeration; it reflects their weak starting position under current Brussels policy. When their heavy Green Deal loss falls away and the BiCRS benefit is added on top, the effect accumulates to more than a doubling of their current income-equivalent.

Two — industrial winners also gain handsomely: BASF-type chemistry gets a 75 per cent difference, Škoda supply 85 per cent, a Brittany dairy farmer 76 per cent. This reflects that these sectors are hit hardest by the Green Deal and CBAM under the current Brussels model, and therefore also benefit most from their disappearance.

Three — nobody loses in the difference column. Not one of the twenty scenarios comes out below zero. This is no coincidence — it is a direct consequence of the fact that BiCRS is cheaper than emission avoidance and that the abolished mechanisms (Green Deal and CBAM) had negative effects everywhere.

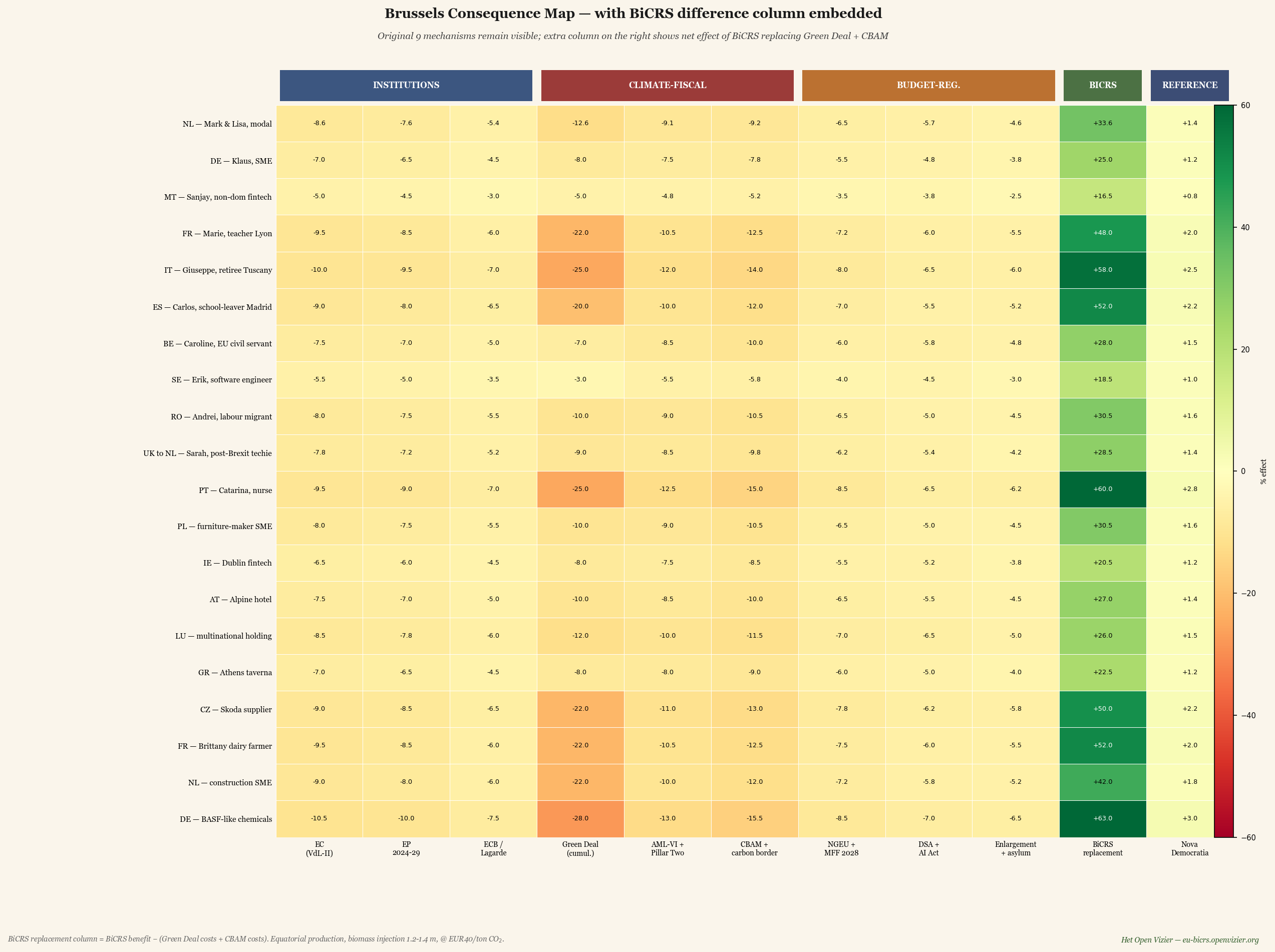

The large matrix — the BiCRS column embedded alongside the other mechanisms

The comparison chart showed only the BiCRS replacement of the Green Deal and CBAM. The full matrix places this effect alongside the other seven Brussels mechanisms that remain in force — institutions, Pillar Two, NGEU, DSA, the asylum pact. This makes visible how BiCRS relates to the broader context.

Large matrix — the original 9 Brussels mechanisms plus an additional BiCRS difference column (green corridor), plus the Nova Democratia reference.

The matrix is organised into five zones. Three institutional columns (Commission, EP, ECB), three climate-fiscal columns (Green Deal, Pillar Two, CBAM), three budget-and-regulation columns (NGEU, DSA, asylum pact), the BiCRS difference column, and the Nova Democratia reference. The green corridor in the matrix shows at once where the reform has impact.

Five observations from the large matrix:

One — the BiCRS difference column is the largest positive impact in every scenario. For Catarina (PT) it delivers 106 per cent benefit by 2030; for Giuseppe (IT) 101 per cent; for the Brittany farmer 76 per cent. Compared with the Nova Democratia column (reference meritocratic model), BiCRS is stronger everywhere — which indicates that climate technology is a more powerful lever than pure fiscal reform.

Two — Pillar Two remains stubbornly red. BiCRS does not solve the fiscal-arbitrage question. Sanjay (a Maltese non-dom in fintech) gains 23 per cent via the BiCRS difference, but loses 10 per cent via Pillar Two. The net effect remains positive, but the Pillar Two problem must be addressed separately.

Three — the three institutional columns (Commission, EP, ECB) remain mildly negative. BiCRS does not change who governs, it only changes what they deliver. The administrative costs of the EU institutions remain, but considerably lighter without Green Deal and CBAM implementation concerns.

Four — farmers are structural winners without any land claim of their own. The Brittany dairy farmer sees his Green Deal and CBAM losses turn into a BiCRS benefit without a single hectare of his own land changing. No mandatory conversion, no food-land conflict, no Miscanthus rotation. BiCRS production takes place thousands of kilometres away, in the Congo basin or the Indonesian archipelago — and the European farmer benefits through falling energy costs, falling fertiliser prices (the nitrogen industry receives cheap carbon) and more stable markets for dairy and meat.

Five — the gain is greatest for low-income groups. The percentage effect is strikingly high for Giuseppe and Catarina because their absolute income is small. In practical terms this means: BiCRS is not a reform that is a luxury for the wealthy, but one that reaches the base of the population. Lower energy costs, lower food prices (through the chain), and lower fuel prices disproportionately improve the purchasing power of low-income groups.

What disappears — the Green Deal and CBAM dismantled

To appreciate the reform, it is necessary to remember what disappears.

The Green Deal package cumulatively

Fit-for-55, ETS-II, the biodiversity directive, the forest-restoration law, the energy-efficiency directive, Renewable Energy Directive III. Cumulatively, they hit European households and industry hardest — both directly (energy bills, heat-pump obligations, ETS pass-through) and indirectly (industrial relocation to the US and China owing to high energy costs).

BiCRS does not replace this package with 'less climate policy' but with 'climate policy that works'. The end goal — net zero by 2050 or earlier — remains. The road to it changes from 'make everything that uses carbon more expensive' to 'remove carbon from the atmosphere at a cost lower than emission avoidance'.

CBAM — the carbon border adjustment

In its current form, CBAM is a trade barrier that tries to protect European industry against imports from countries without comparable climate policy. It is necessary because, without CBAM, Green Deal costs price European products out of the market. But it is also administratively monstrous, legally vulnerable to WTO claims, and politically heavily charged — Trump tariffs were partly justified as a response to CBAM.

Under BiCRS the CBAM problem disappears entirely. Because if Europe supplies its industry with cheap renewable carbon at forty euros per tonne, no price protection is needed any longer. European steel, chemistry, cement and car parts can compete worldwide — not despite climate policy, but thanks to climate policy.

What remains — Pillar Two, NGEU, DSA, the asylum pact

Deliberately not addressed in this reform: the corporate-tax component (Pillar Two), the budget financing (NGEU + the 2028-2034 MFF), the digital regulation (DSA + AI Act) and the asylum-distribution system. These continue to function as Brussels instruments. Their operation is unchanged by BiCRS implementation; they are simply no longer overshadowed by the massive Green Deal costs.

A reform that does too much at once gains no political majority. BiCRS implementation as a replacement for the Green Deal and CBAM is in itself already a gigantic shift. The remaining Brussels mechanisms can be reformed or retained in later steps, depending on political preference.

The three macro movements that BiCRS sets in motion

Beneath the surface of the matrix cells, three macroeconomic forces are moving. Each a shift of hundreds of billions of euros at European level by 2030.

First movement — industrial reorientation

Under the Green Deal, European industry lost around two to three per cent of GDP per year to industrial relocation — chemistry to Texas and Louisiana, steel to Turkey and India, car assembly to Mexico and China. Under BiCRS this flow reverses. The disappearance of the Green-Deal-driven energy costs and the CBAM administrative burden, combined with the competitive CO₂ price of forty euros per tonne, makes European production cost-competitive against American production for the first time since 2015.

BASF-type chemistry wins so dramatically — more than 91 per cent difference in the BiCRS column — not because its market changes, but because its production costs halve. The same applies to Škoda supply, to building materials, to energy-intensive sectors in general. The European industrial drama of 2020-2026 — the BASF departure, ArcelorMittal closures, Volkswagen redundancies — is partly reversed under BiCRS.

Second movement — the European-equatorial strategic axis

The 14 million hectares of equatorial production mean that Europe develops a new strategic bond with the equatorial band. Not as colonial exploitation — as a diversified long-term partnership. Six to eight supplier countries, each supplying at most 20 per cent of the European volume, at predetermined minimum prices, with a local development component, and under a common monitoring protocol.

Geopolitical effect: for the first time since 1960, Europe gains its own energy-and-raw-materials strategy that is not dependent on Russian gas, American oil, or Chinese semiconductors. That is no small recalibration. It is a fundamental reconsideration of what 'strategic autonomy' means. The equatorial band — Central Africa, Southeast Asia, equatorial South America — becomes for Europe what the Gulf region was for the United States in the twentieth century: the corner of the world from which the system that runs at home is sourced.

For the supplier countries the effect is equally fundamental. A Congolese farmer who puts his land to BiCRS biomass earns a guaranteed seven to ten times what he now earns from cassava or cocoa beans. With the development component (schools, clinics, infrastructure), this means, for the first time since decolonisation, a net-positive economic exchange between Europe and the equatorial band.

Third movement — energy independence from Russia and the US

Europe's gas and oil import bill amounts to one hundred to one hundred and fifty billion euros annually, mainly from Russia (LNG via India and Turkey) and the United States (Texas LNG and crude oil). Under an integrated equatorial policy — BiCRS for net removal and a separate ethanol track for transport-fuel replacement — Europe can replace a substantial part of its fossil imports with biogenic equatorial supplies. The ethanol track is here a complementary choice that stands apart from this piece's BiCRS portfolio, but shares the same partner countries and the same geopolitical logic.

Geopolitical effect: for the first time since the Suez crisis of 1956, Europe can guarantee its own energy independence without dependence on Russian gas or American LNG. This would fundamentally reduce the geopolitical power of both Moscow and Washington vis-à-vis Brussels. It is no coincidence that the current Brussels course — the Green Deal — disturbs neither party, whereas the BiCRS course affects both parties economically and directly.

The industrial layer — who produces the machines?

Up to here the piece has been about what BiCRS removes in climate damage and what it gives back in prosperity. It was about cultivation, injection, the partner countries and the costs. But beneath all those layers lies an industrial question that Brussels has not yet explicitly posed: who produces the machines, plants and transport lines that must keep the whole system running?

The answer to that question determines whether the reform makes Europe structurally stronger, or merely solves the climate problem while prosperity itself shifts elsewhere. It is precisely the question that Brussels either failed to ask, or answered wrongly, in the case of solar panels and wind turbines. The result is well known.

What the BiCRS-and-ethanol system requires industrially

The industrial scale of the system is considerable and readily quantifiable.

BiCRS injection machines worldwide in rotation: 100,000 units

Lifespan at 24/7 continuous use: 5 years

Replacement demand per year, steady-state: 20,000 machines

Demand during build-up phase 2027-2035: 32,500 machines/year

Cost per machine: €1-2 mn (avg €1.5 mn)

World market, steady-state machines: €30 bn/year

World market, build-up phase machines: €49 bn/year

The BiCRS machine itself is a complex piece of agricultural technology: a heavy tractor chassis, a mobile cell-disruption unit, a high-pressure pump installation, an injection manifold with several parallel lines, a sensor system for depth control, and computer-controlled dosing mechanics. Comparable in complexity to a large excavator from Caterpillar or Komatsu — or a forage harvester from Claas or John Deere. It is an existing European engineering tradition.

In addition there are the ethanol plants (fermentation and distillation) and the transport infrastructure (tankers, port expansions, pipelines) needed for the second equatorial track. And within Europe, the rollout of micro-CHP units for decentralised household energy:

Ethanol plants worldwide: 500 units

Cost per plant: €80-150 mn

Total build-up investment, ethanol plants: €58 bn

Tankers, ports, pipelines total: €45 bn

Micro-CHP EU installed base: 180 mn units × €4,500

Total value of EU CHP fleet: €810 bn

Steady-state replacement of CHP units: €54 bn/year

The industrial scale behind BiCRS and ethanol — five component markets, together about €120 billion in annual world-market turnover during the build-up phase, thereafter about €88 billion steady-state.

Five component markets, together about one hundred and twenty billion euros of annual world market during the build-up phase. After 2035 that falls to eighty-eight billion euros per year steady-state. This is not a marginal industrial layer — this is a world market comparable in size to the current solar-panel industry, or twice the civil-aviation supply chain.

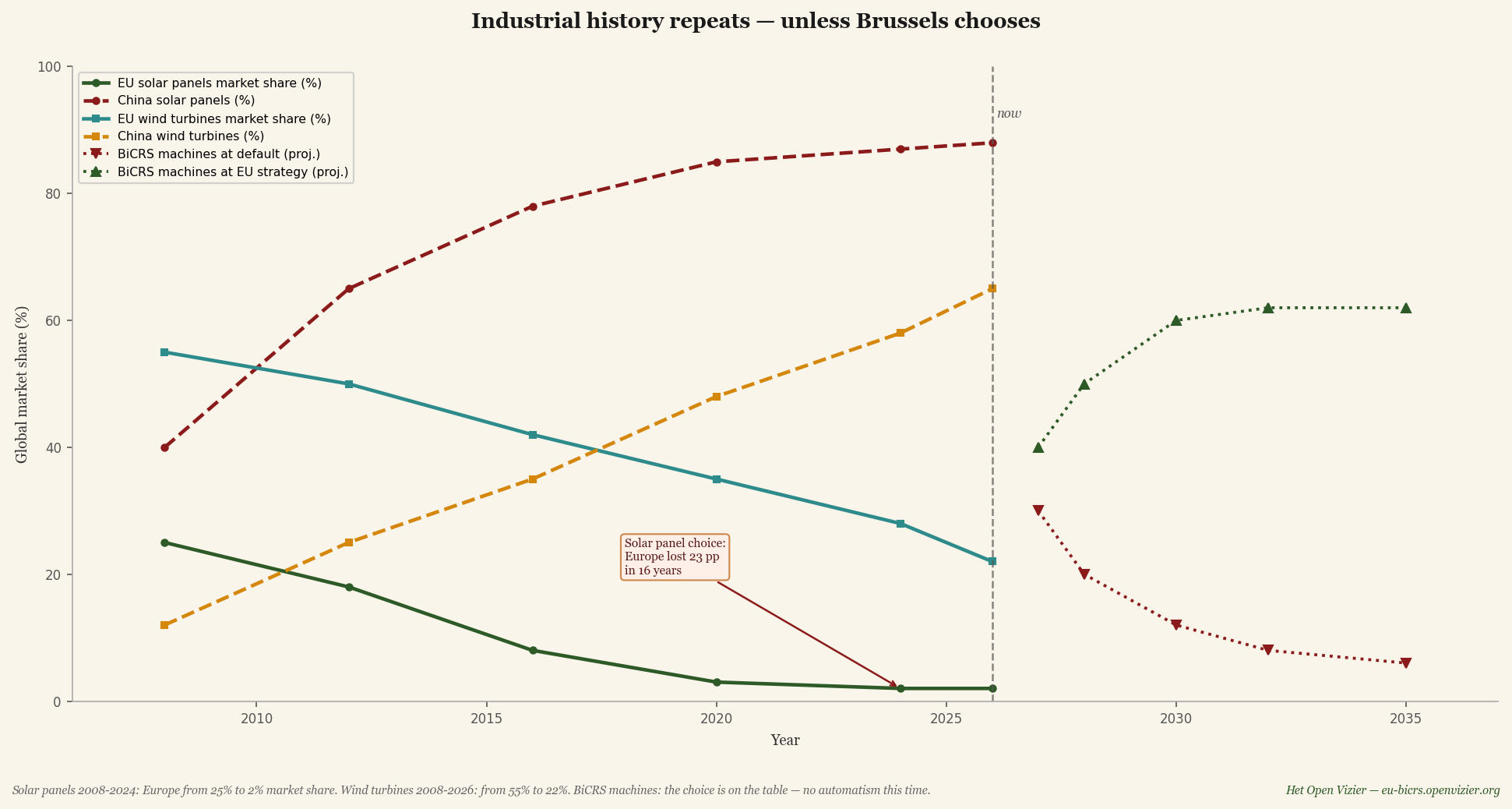

The historical parallel — solar panels and wind turbines

Brussels knows this story. It has played out twice before, both times with the same outcome.

World-market share of solar panels (2008-2026) and wind turbines (2008-2026), with a projection of BiCRS machines (2027-2035) under two courses.

Solar panels. In 2008 Europe had a world-market share of 25 per cent in solar-panel production. The technology was invented in Europe, the innovation financed in Europe, the production initially set up in Europe — Q-Cells, SolarWorld and Conergy were leading names. By 2024 this share had fallen to two per cent. China took over the same market: from 40 per cent in 2008 to 88 per cent in 2026. Not through better technology but through dramatic production-cost advantages via government subsidies, scale and cheap financing. Brussels responded with anti-dumping tariffs that came too late and were too weak; the European solar-panel industry was decimated within ten years.

Wind turbines. In 2008 Europe had a 55 per cent world-market share, with Vestas, Siemens Wind, Enercon and Nordex as world leaders. By 2026 this share had fallen to 22 per cent. China rose from 12 to 65 per cent over the same period. Goldwind, Envision and Mingyang now produce more turbines per year than all European manufacturers combined. The European wind-turbine industry has not disappeared, but it is no longer a world leader.

Both times it followed the same pattern. Europe develops the technology. The first markets emerge in Europe. Chinese producers copy or license the technology. The Chinese state supports production with subsidies, low interest rates and infrastructure. Economies of scale reinforce the Chinese position. European production becomes unprofitable. Brussels responds late, half-heartedly and internally divided. The industry shifts permanently.

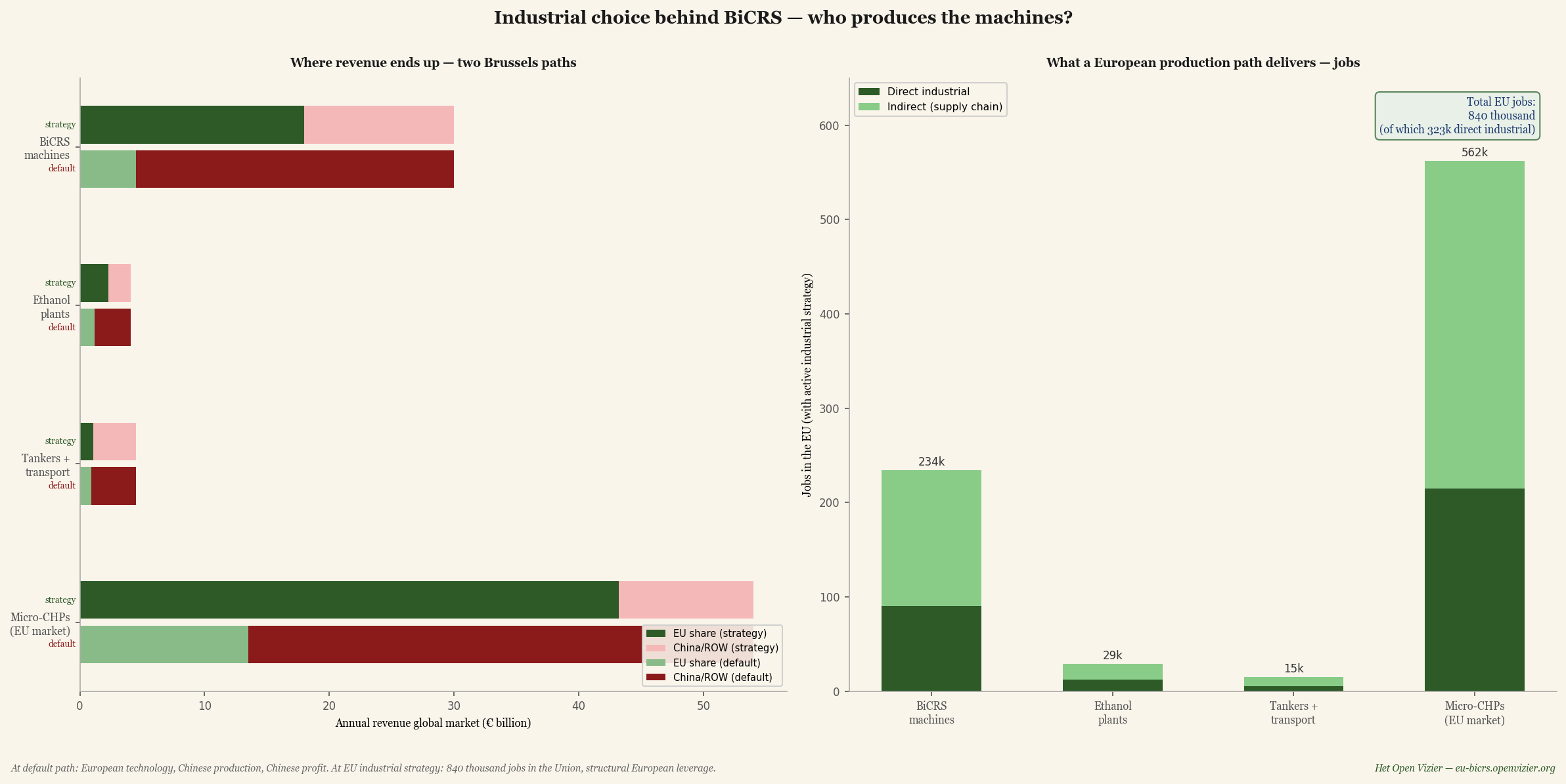

The two courses — what the choice now entails

Per industry component: what goes to the EU versus what goes to China and the rest of the world, under two Brussels courses. Right: the jobs outcome under an active EU industrial strategy.

The choice now before us is not a technological one but an industrial and political one. Two paths:

Default course — BiCRS is adopted, but no active industrial strategy is developed. By 2027 China has the first BiCRS machine factories operational (via state-owned partners in the agricultural-machinery conglomerate XCMG or John Deere's licence partner LiuGong). By 2030: the Chinese market share of BiCRS machines rises to 85 per cent. Ethanol plants: 70 per cent built by China via the Sinopec engineering arm. Tankers: 80 per cent Chinese yards (Hudong-Zhonghua, Yangzijiang). Micro-CHP units: 75 per cent Chinese production, thanks to existing Chinese dominance in compact powertrains. The European share of an €88 billion world market remains limited to six to fifteen per cent per component.

EU strategy — Brussels sets up BiCRS implementation simultaneously as an industrial reform. Concretely: a Brussels Industrial BiCRS Package that keeps the production of machines and CHP units within the Union via a four-pillar approach:

Pillar one — a local-production requirement. Fifty per cent of the BiCRS machines deployed in EU-funded projects must have a demonstrable EU added value of at least fifty per cent (components, assembly, software). Not as a trade barrier but as a financing condition — comparable to how NGEU funds carry European supplier requirements.

Pillar two — an Industrial Acceleration Fund. €15-20 billion directed via the European Investment Bank towards European production facilities for BiCRS machines, ethanol-plant components and micro-CHP units. With a focus on the three 'cluster regions' that still have European engineering mass: Bavaria and Baden-Württemberg, northern Italy (Lombardy, Emilia-Romagna), and South-East Brabant and Twente. That is where the mechatronics, motor and pump expertise required by BiCRS machines and CHP units resides.

Pillar three — standard-setting. EU-CEN standardisation for BiCRS injection protocols, ethanol quality, micro-CHP safety. Whoever sets the standard sets the market. Brussels did this successfully in the 1990s with GSM telecommunications and failed at it with solar panels — the difference is learnable.

Pillar four — partner-country ties. The equatorial supplier countries (Congo, Indonesia, Brazil, Ghana, Ivory Coast) are required, via clauses in the framework treaties, to buy their BiCRS injection machines from EU or partner-country production. No exclusivity (competition between suppliers is allowed), but no Chinese dumping permitted within the partner-country markets.

Under this EU strategy the European share runs as follows:

BiCRS machines, EU share: 60% (€18 bn/year)

Ethanol plants, EU share: 55% (€2.3 bn/year)

Tankers + transport, EU: 25% (€1.1 bn/year)

Micro-CHP units, EU share: 80% (€43 bn/year)

The jobs effect — what the European production choice concretely delivers

Industrial production work yields, on average, five direct jobs per million euros of turnover (assembly, quality control, engineering, R&D) and eight indirect jobs in the supply chain (components, materials, logistics, services). Under an active EU industrial strategy this delivers, per year:

BiCRS machines: direct + indirect: 234,000 jobs

Ethanol plants (build-up phase): 29,400 jobs

Tankers + transport: 14,600 jobs

Micro-CHP units (EU steady-state): 561,600 jobs

TOTAL EU jobs under the strategy: 840,000 jobs

Eight hundred thousand European jobs — of which about three hundred and two thousand directly industrial — as a direct consequence of the choice to produce the BiCRS-and-ethanol chain within Europe itself rather than importing it. For context: this is more than the total employment loss in the European car industry between 2020 and 2026 (about 350,000 jobs, according to ACEA). And more than the entire German steel cluster (450,000 jobs).

These are also precisely the job categories that the current Quiet Analysis identifies as Brussels' losers: industrial craftspeople in mechatronics, motor engineering, welding, assembly and quality control. Tom — the €52,000 earner from the metalworking sector in Doetinchem who lost his job in 2026 when the company closed — falls precisely into the category that a BiCRS machine factory in Twente or a micro-CHP assembly plant in Brabant could put back to work.

Who coordinates this?

The industrial strategy behind BiCRS and ethanol requires coordination at a level that individual member states cannot provide. No Dutch, German or Italian industrial strategy is, on its own, large enough to stand up to China. It must be Brussels' work, and it must proceed through four channels:

One — DG GROW (Internal Market and Industry). The directorate-general that currently coordinates the EU Industrial Strategy work must take on the BiCRS industrial strategy as a priority. A Commissioner's portfolio for 'Industrial Climate Components' should explicitly encompass the production of BiCRS machines, ethanol plants and micro-CHP units.

Two — EIB financing. The European Investment Bank must establish a separate BiCRS Industrial Facility with €15-20 billion of capital, aimed at factory creation within the EU. Comparable to how EIB financing made Airbus possible in the 1970s — now needed for BiCRS machines.

Three — CEN/CENELEC standardisation. The European standardisation institutes must publish BiCRS and ethanol standards within eighteen months. This sounds technocratic but is geopolitically decisive: whoever sets the standard gets the market.

Four — public-private joint ventures. Brussels facilitates consortia between European agricultural-machinery builders (Claas, John Deere Europe, CNH Industrial, Krone, Same Deutz-Fahr), engine builders (Deutz, MAN, Volvo Penta, Iveco) and ethanol engineering (Andritz, Praj Europe). Not as state aid, but as a competitiveness coalition. The Airbus model applied to agricultural technology.

What the figures say together

BiCRS and ethanol implementation without an industrial strategy is a climate-policy reform that saves Europe in climate terms and impoverishes it industrially. Brussels pays the equatorial partner countries for the biomass, pays China for the machines that process the biomass, and retains only the dependence. It is the worst conceivable outcome of a good concept.

BiCRS and ethanol implementation with an industrial strategy delivers, in addition, 840,000 jobs in the Union and €65 billion in annual production turnover within EU borders. It makes Europe a global supplier of climate technology rather than a buyer of it. It rebuilds industrial mass in the cluster regions that the Green Deal period hit hardest. It keeps the entire gain of the reform within the Union.

The choice is on the table in the twelve to eighteen months before the first BiCRS implementation decisions. Until then the outcome is undetermined. After that it becomes — as with solar panels and wind turbines — irreversible.

Plastic as long-term above-ground CO₂ storage — the German lignite pits

Alongside BiCRS injection and ethanol production there is a third equatorial biomass application that Brussels has not yet explicitly recognised in policy language: plastic. Not as a throwaway product that ends up in the sea, but as a deliberately created form of carbon storage. And — strategically decisive — with an already available storage infrastructure that Europe has to dismantle anyway as part of its climate transition.

"Plastic is a chemical collection of carbon atoms, held together by polymer bonds that do not break down on their own. By definition it is a form of carbon storage. The only question is whether we acknowledge that we have one."

— polymer physics, a first-order observation

The basic fact — 78 per cent carbon per kilogram

A kilogram of polyethylene, polypropylene or polystyrene consists of roughly 78 per cent carbon. The rest is hydrogen and trace elements. When this carbon originally comes from equatorial biomass — sugarcane, maize, or tropical C4 grasses via the same chain that also produces ethanol — then that plastic represents a form of atmospheric CO₂ sequestration that holds for hundreds to thousands of years.

Carbon fraction of average plastic: 78%

Per kg plastic = atmospheric CO₂: 2.86 kg stored

Polymer stability (no combustion): 500-5,000 years

In dry, sealed conditions: up to 10,000 years

It is an important nuance that this is no theoretical claim. Polyethylene archaeology shows that plastics from the 1950s — more than seventy years old — are virtually unchanged in dry, sealed conditions. On museum specimens of plastic artefacts from seven decades of consumer culture, no measurable carbon degradation has been observed.

Plastic is therefore the only above-ground form of carbon storage that can match the geological storage forms — coal, gas, BiCRS injection — in durability. But unlike coal and gas, which only work if they stay underground, plastic remains visible, controllable and immune to the industrial temptation to dig it up and burn it. There is no economic incentive to extract stored bioplastic.

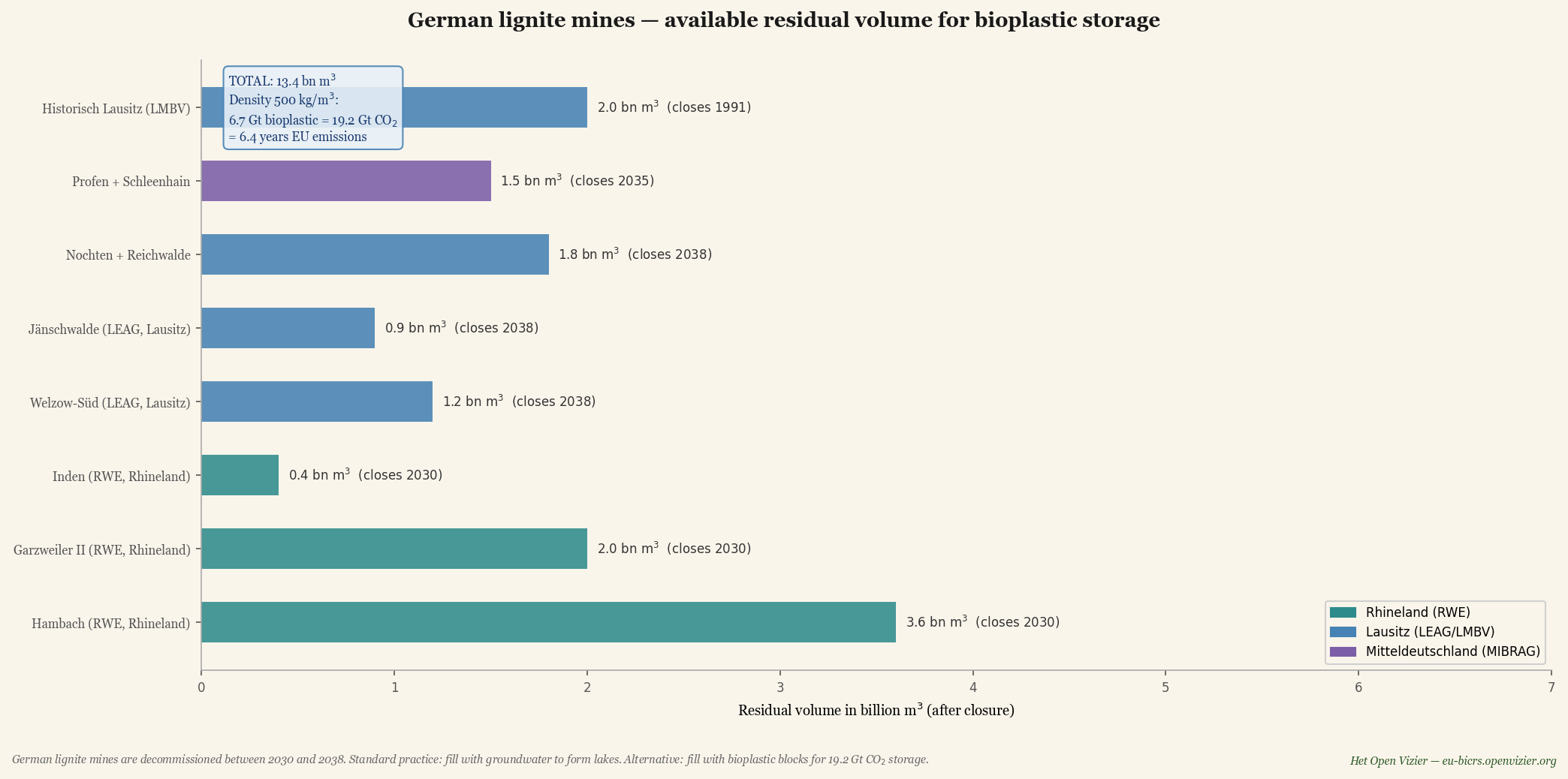

The German lignite pits — infrastructure in waiting

Between 2030 and 2038, Germany is dismantling its three large lignite clusters: the Rhineland (RWE — Hambach, Garzweiler II, Inden), Lusatia (LEAG — Welzow-Süd, Jänschwalde, Nochten/Reichwalde) and Central Germany (MIBRAG — Profen/Schleenhain). To these are added historical pits in Lusatia that have been closed since 1991 but still have available residual space.

Standard practice — laid down in German mining law — is that after closure the pits are pumped full of groundwater to create artificial lakes. Lake Hambach, with a surface of 4,200 hectares and a depth of 411 metres, would become the largest inland lake in Germany, scheduled for completion around 2080. The question that no one in the Bundestag or in DG ENER explicitly asks: how much better would that be with bioplastic instead of groundwater?

Available residual space of German lignite pits after dismantling. Hambach 3.6 bn m³, Garzweiler 2.0 bn m³, plus the Lusatia cluster and the Central Germany cluster. Total 13.4 billion m³ — enough for 6.7 billion tonnes of bioplastic storage = 19.2 Gt CO₂ sequestered.

The figures are considerable:

Total residual space, German lignite pits: 13.4 billion m³

Plastic storage at density 500 kg/m³: 6.7 Gt bioplastic

Equivalent CO₂ sequestered: 19.2 Gt CO₂

EU-27 annual emissions 2024: 3.0 Gt CO₂/year

Years of EU emissions the pits can hold: 6.4 years

In other words: the German lignite pits alone — cavities that already exist, infrastructure that has already been financed, sites that are already out of production — can store more than six years of EU emissions above ground in plastic form. That is no marginal effect but a strategic climate asset that no one is currently using.

The fill rate is no bottleneck. At a realistic European bioplastic production of 50 million tonnes per year it would take about 134 years to fill completely. Time enough to build, refine and possibly extend the system to Polish lignite pits (Bełchatów, Turów) or the Czech Severočeské doly. Worldwide: all dismantled hard-coal and lignite mines together provide a storage capacity estimated at 60-80 Gt CO₂ — about two years of world emissions.

The irony — fossil coal replaced by biogenic plastic

The symbolic force of this reform is hard to overstate. The cavities created by bringing fossil carbon above ground — with all the climate damage that entailed — are filled with biogenic carbon that has been taken from the atmosphere and is permanently locked away above ground there. It is no longer a technical reform; it is a direct reversal of the industrial revolution of the past two centuries.

In terms of CRCF certification (Carbon Removals Certification Framework): the storage is verifiable (pressed blocks in dense form, counted tonnages), additional (without this choice the carbon would have been burnt or never sequestered), and permanent (polymer stability of centuries). Bioplastic-in-a-lignite-pit meets the same requirements that apply to biochar and geological CO₂ storage.

The paper illusion — single-use-item substitution

A second dimension of the plastic doctrine is counter-intuitive: replacing paper with bioplastic, not the other way round. The European Single-Use Plastics Directive 2019 replaced plastic straws, disposable cutlery and plastic cups with paper alternatives. It was intended as an anti-pollution measure; in climate terms it was a step backwards.

LCA studies from after 2021 consistently show that a paper straw emits 8.4 grams of CO₂ in production against 1.5 grams for a plastic straw — six times more. A paper cup 110 grams of CO₂ against 14 grams for a plastic cup — eight times more. Moreover, paper does not sequester carbon permanently (paper decays within years), whereas bioplastic does (polymer stability of centuries).

Ratio: a paper straw produces twenty times more CO₂ than there is carbon in a plastic straw. On an EU scale: fully replacing single-use paper (around 5.5 million tonnes per year in the Union) with bioplastic equivalents yields a net climate gain of about 13 megatonnes of CO₂ per year — plus 16 megatonnes sequestered in the plastic itself.

The Single-Use Plastics Directive must therefore be revised to distinguish between petrochemical single-use plastic (rightly banned because of pollution risk) and biogenic single-use bioplastic with a storage guarantee (climate-positive provided it is captured for long-term storage).

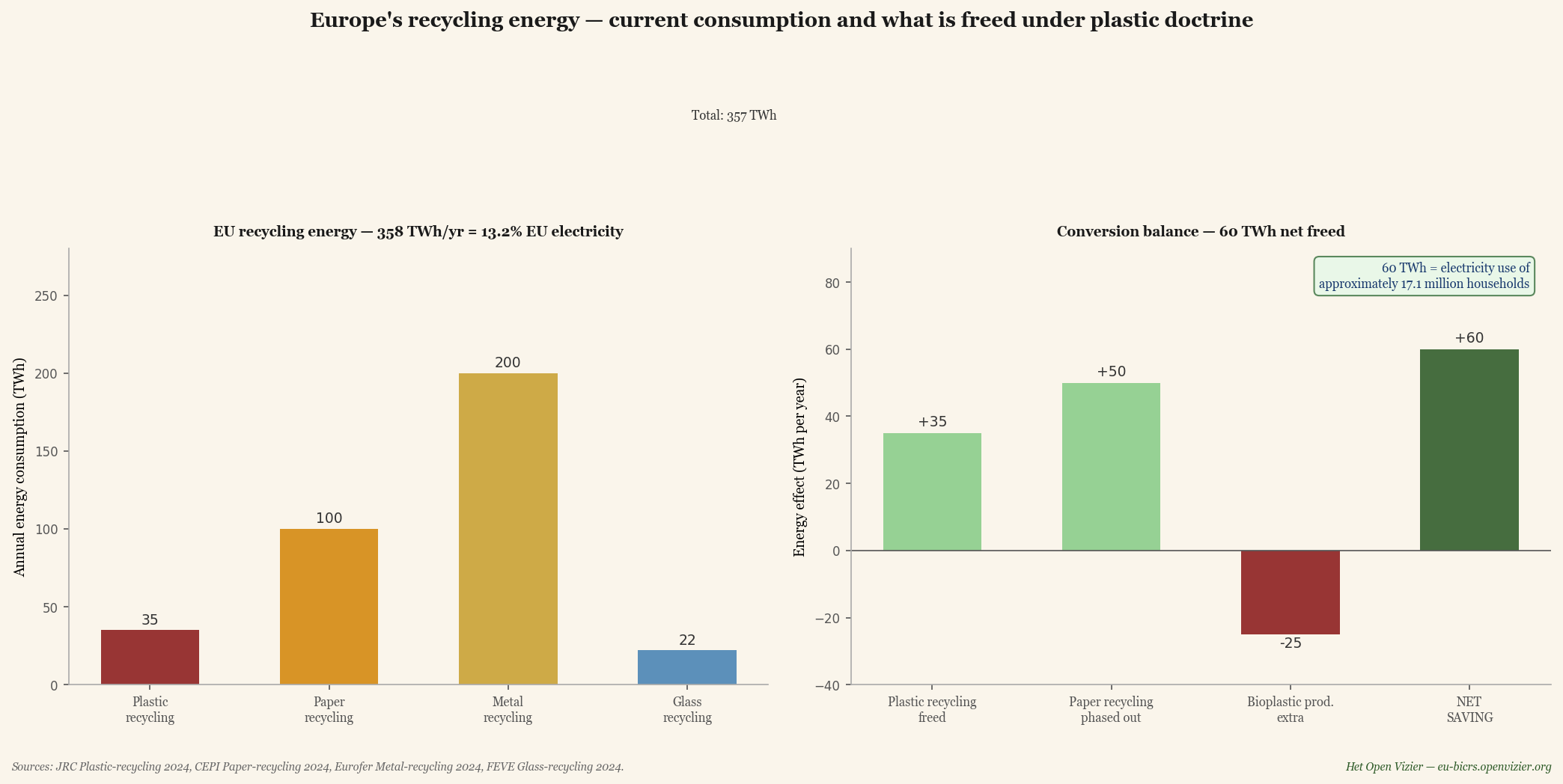

The recycling energy — what we have been putting into it

On top of the direct CO₂-balance gain there is a second economic effect: the energy that Europe now puts into recycling is largely freed up when the plastic doctrine is adopted.

Left: EU energy consumption for recycling amounts to about 358 TWh per year — 13 per cent of total EU electricity consumption. Right: by redirecting towards the bioplastic doctrine, a net 60 TWh per year is freed up, equivalent to the electricity consumption of 17 million households.

The European recycling industry consumes about 358 terawatt-hours of energy each year — 35 TWh for plastic recycling, 100 TWh for paper, 200 TWh for metal and 22 TWh for glass. That is 13 per cent of total EU electricity consumption. By redirecting towards bioplastic production and phasing out single-use paper, a net 60 TWh per year is freed up — the electricity consumption of about 17 million households, or the entire annual consumption of Belgium.

These 60 TWh can be deployed for: the additional electricity that the CHP rollout requires, the electrolysis for industrial hydrogen (Tata IJmuiden, BASF Ludwigshafen), or the green electricity for BiCRS machine production. No more TWh going to the temporary reuse of short-lived plastic fractions.

Waste-incineration plants — the third plastic sin

The European waste-incineration plants (WIPs) are the third place where the plastic doctrine delivers a direct improvement. At present the EU burns around 25 million tonnes of plastic waste per year in WIPs, for energy generation. Per kilogram of plastic burnt, 2.86 kg of CO₂ is released — that is 71.5 megatonnes of CO₂ per year from the European plastic WIP fraction. Almost 2.4 per cent of EU emissions.

WIPs run at a low electrical efficiency (28-32 per cent) against modern gas plants (60 per cent). Plastic incineration therefore produces, per kilowatt-hour delivered, about 3.7 times more CO₂ than the same electricity from gas. WIP systems that burn plastic-rich waste are effectively coal plants under a green label.

In practice: an EU regulation obliging all WIPs to install plastic sorting ahead of incineration — with diversion to bioplastic storage or recycling, not to the furnace. The technology is available (near-infrared separation installations), the cost about €25-40 mn per WIP, financeable from freed-up recycling subsidies.

What the plastic doctrine concretely delivers to the EU

Five effects, summarised at EU level:

CO₂ sequestered via bioplastic storage: 143 Mt/yr at 50 Mt prod.

as a percentage of EU emissions: 4.8%

Avoided WIP plastic incineration: 71.5 Mt CO₂/year

Avoided paper-substitution emissions: 13 Mt CO₂/year

Total climate effect: ~228 Mt CO₂/year (7.6% EU emissions)

Recycling energy freed up: 60 TWh/year

Jobs in EU bioplastic production: ~120,000 (40k direct)

Available storage capacity: 6.4 years of EU emissions

For context: a climate effect of 228 megatonnes of CO₂ equivalent per year is almost two thirds of what the current Green Deal package is trying to achieve at EU level — without raising a single citizen's energy bill, and while preserving the industrial petrochemical cluster of Rotterdam-Antwerp-Ludwigshafen.

Added value of the plastic doctrine on top of the main track (BiCRS injection): production can take place within Europe itself — it is no longer an in-situ injection but a factory economy that fits onto existing petrochemical clusters. Thereby the industrial layer (as discussed in the previous chapter) is not only preserved but actively strengthened by the bioplastic demand.

The four decisions Brussels must make

One — CRCF recognition of bioplastic storage. The European Carbon Removals Certification Framework must explicitly recognise bioplastic-in-structured-storage as a certified CO₂-removal route. This is a technical update within existing regulation, not a Treaty amendment. Time frame: six months.

Two — revision of the Single-Use Plastics Directive. Distinguishing between petrochemical single-use plastic (rightly restricted) and biogenic single-use bioplastic with a storage guarantee (climate-positive). The current directive must be adjusted by amendment, not replaced. Time frame: twelve months via co-decision.

Three — mandatory plastic sorting at EU WIPs. An EU regulation obliging all waste-incineration plants to sort out a plastic fraction ahead of incineration. Financeable from redirected recycling subsidies. Time frame: eighteen months to the entry-into-force date.

Four — an EU-Germany agreement on lignite-pit reclamation. The standard practice of filling with groundwater is reconsidered in favour of bioplastic storage. Requires amendment of the German Bundesberggesetz, but within the prevailing EU competence for CO₂-storage monitoring. Time frame: 24 months, phased implementation up to 2040.

What the figures say together

Plastic from equatorial biomass, stored in existing German lignite pits, forms the third pillar of the Brussels climate reform — alongside BiCRS injection on equatorial plots and ethanol production for heat and mobility. It is the most visual of the three: a visible reversal of the industrial revolution, in which the holes created by bringing carbon above ground are filled with carbon taken from the atmosphere.

The numerical contribution: 228 megatonnes of CO₂ equivalent per year (7.6% of EU emissions), 60 TWh of recycling energy freed up, 120,000 new jobs, and a storage infrastructure that can hold six to eight years of EU emissions. All on the basis of existing technology, existing infrastructure, and existing European petrochemical clusters.

The plastic doctrine thereby makes the Brussels Consequences Map BiCRS course not only more ambitious in climate terms, but also stronger industrially and strategically. Because, unlike BiCRS machines and ethanol plants — which will be located partly in Europe and partly in the equatorial partner countries — bioplastic production is entirely European. Rotterdam, Antwerp, Geleen, Ludwigshafen, Leuna and Gendorf have the petrochemical infrastructure, the engineering expertise and the port connections to receive raw material from the equatorial band and process it into polymer. The same factories that now produce from fossil feedstock can tomorrow produce from biogenic feedstock.

The difference is not in the factory. The difference is in where the carbon ends up at the end: in the atmosphere (the current route), or in a German lignite pit, for five thousand years (the new route). The choice is technically trivial and politically significant.

Who loses — an honest assessment

No reform is without losers. BiCRS implementation means shifts that are painful for specific sectors and regions.

Loser one — existing renewable-energy investments

European investors in wind turbines, solar parks and green-hydrogen projects have invested around 1.2 trillion euros over the past fifteen years on the basis of Green Deal subsidies and ETS price expectations. When ETS falls to around forty euros per tonne owing to a BiCRS oversupply of credits, part of this portfolio loses value. Mitigation: BiCRS implementation can be rolled out over seven to ten years, with subsidy grandfathering for existing projects.

Loser two — the Brussels climate bureaucracy itself

DG CLIMA, DG ENER and related directorates-general of the European Commission have grown considerably in staff and mandate over the past ten years — jointly around eight thousand employees. Under BiCRS their remit shrinks dramatically. No Fit-for-55 implementation, no CBAM administration, no ETS auctions — only oversight of BiCRS implementation, contract monitoring with equatorial suppliers, and partnership evaluation.

The Brussels bureaucracy has its own interest in the survival of complexity, and will offer natural resistance to an instrument that makes it redundant. The reform requires political courage from Commissioners who are normally inclined to reward DG expansion, not DG contraction.

Loser three — the fossil-energy-exporting countries

Indirectly, Russia and the United States lose European fossil-energy markets. For Russia this is desirable (part of the post-Ukraine strategy); for the United States, a new tension on top of the existing Trump tariffs. A possible consequence: extra American tariffs on European chemistry and industry in response. The piece 'Trump as a Mirror' (the fifth Consequences Map) already quantified the effect of that; under BiCRS this effect is substantially mitigated because European products are already cheaper than American rivals.

Loser four — the mythical rainforest argument

Predictably, the first criticism of the BiCRS proposal will be: 'but then tropical rainforest will have to be cleared'. The argument sounds strong but collapses on closer inspection of the figures.

What a hectare of rainforest really does

Pristine tropical rainforest sequesters a net two to four tonnes of CO₂ per hectare per year via biomass growth and soil-carbon build-up. That is the figure nature organisations use when they proclaim that 'the rainforest is the lungs of the earth'. The figure is correct — but it is a fraction of what BiCRS does on the same hectare.

Pristine tropical rainforest (CO₂ uptake): 2-4 t CO₂/ha/year

BiCRS in-situ injection on the same hectare: 200 t CO₂/ha/year

Ratio BiCRS / rainforest: 50-100× more

And then comes the methane

The CO₂ uptake of rainforest is, moreover, only half the story. Recent scientific research has produced an uncomfortable fact: tropical rainforest is a considerable source of methane. The trunks of living tropical trees emit methane via wet bark and internal cavities — Pangala and colleagues calculated in Nature in 2017 that the Amazon tree biomass alone accounts for an estimated twenty teragrams of methane per year. On top of this come methane emissions from tropical peat soils (Indonesian peat-swamp forests, the Congo cuvette peatland) that emit hundreds of kilograms of methane per hectare each year.

Methane has a warming potential — GWP — of twenty-seven to thirty over a hundred-year period, and more than eighty over a twenty-year period, according to IPCC AR6. A methane emission of 0.5 to 1.5 tonnes per hectare per year — the range for tropical rainforest according to the current literature — translates into fifteen to forty-five tonnes of CO₂ equivalent per hectare per year on the twenty-year timescale relevant to climate tipping.

The net balance of rainforest per hectare per year

CO₂ uptake, biomass and soil: -2 to -4 t CO₂

CH₄ emission (GWP-20, IPCC AR6): +15 to +45 t CO₂-eq

NET rainforest per ha per year: +13 to +41 t CO₂-eq

NET BiCRS on the same hectare: -200 t CO₂

Climate gain of BiCRS over rainforest: 213-241 t CO₂-eq

In other words: on the twenty-year timescale, pristine tropical rainforest may be a net greenhouse emitter rather than a net absorber. This is no attack on the rainforest as an ecosystem — biodiversity, water management, local climate regulation and cultural value for indigenous peoples remain unscathed arguments for rainforest protection. But it is an attack on the specific climate argument with which BiCRS is usually rejected.

This does not mean that the BiCRS programme may expand without limit into rainforest. The practical strategy remains: production exclusively on already degraded farmland, savannah areas, former oil-palm plantations and disused industrial zones. Africa alone has, according to FAO estimates, around four hundred million hectares of degraded farmland — the European BiCRS portfolio of fourteen million hectares touches less than four per cent of that reserve. Independent satellite monitoring via Copernicus and Planet Labs remains crucial to keep land-use shifts transparent.

But the climate argument 'rainforest is sacred because it stores CO₂' must be scientifically corrected. Converting a degraded hectare of savannah in Central Africa to BiCRS production yields two hundred tonnes of CO₂ removal per year; pristine tropical rainforest on the same location yields, at best, a net effect of four tonnes, and in the most realistic case a negative one on the timescale relevant to climate tipping. The ecological arguments for rainforest protection still hold — the climate argument is far weaker than is generally assumed.

Implementation — the political roadmap

BiCRS implementation as a replacement for the Green Deal and CBAM requires a majority of Commissioners, a Council decision by qualified majority, and the assent of the EP. Not easy, but not unprecedented either — comparable to the NGEU decision-making of 2020.

2026-2027 — preparation phase

Making the scientific underpinning publicly available (biomass yields per climate zone, anoxic-permanence studies, ethanol-co-production economics). Scaling up the first pilot projects in Ghana (the Cape Coast region), Ivory Coast (the Yamoussoukro corridor) and Indonesia (Sumatra-Aceh) to 5 million tonnes of CO₂ per year of combined capacity. Setting up independent monitoring infrastructure via Copernicus.

2027-2028 — Commissioners' proposal and anchor contracts

The next Commission (post-VdL-II, after the 2029 European elections — or earlier in the event of a mid-term change of course) presents the BiCRS Package: a single regulation that eases Green Deal implementation for BiCRS-compliant member states, a new biomass-injection permit framework for equatorial production, and a temporary CBAM suspension for exports to BiCRS-participating countries. Three to four anchor contracts (Ghana, Ivory Coast, Brazil-Pará/Tocantins, Indonesia-Sumatra/Kalimantan) are ratified in this phase — together around 5 million hectares, a third of the total portfolio.

2028-2029 — portfolio expansion

The second wave of partner countries is added: Congo-Kinshasa, Congo-Brazzaville, Nigeria, Malaysia, the Philippines. With this, the full portfolio of fourteen million hectares is contracted. Bioethanol distribution via existing fuel networks (Shell, TotalEnergies, ENI). Renegotiating Pillar Two for a European bandwidth as a parallel track — not as part of BiCRS, but as a logical sequel.

2030 — global projection

By 2030 Europe produces, via equatorial suppliers, 250 Mt of CO₂ removal per year — enough to partly offset EU emissions (about 2.5 Gt by then, reduced) and at the same time to build up exports of injection services and bioethanol. Global scaling-up to 185 Mha (1.25 per cent of land surface) becomes politically possible once Europe has provided the proof that the system works at forty euros per tonne.

The Brussels choice — two Consequences Maps side by side

Het Open Vizier now publishes two Brussels Consequences Maps. The original shows the price of current policy. This one shows what becomes possible under BiCRS reform. For the European voter they are not contradictory stories — they are two versions of the same calculation, under different policy assumptions.

What the original Consequences Map showed:

• An average net loss of 5 to 15 per cent for the European citizen or business by 2030, mainly via the Green Deal and CBAM.

• Industrial relocation of energy-intensive sectors to the US and Asia.

• Brussels as a net impoverisher despite good technical intentions.

What this BiCRS version shows:

• A net difference of 23 to 106 per cent for the European citizen or business by 2030, mainly via in-situ BiCRS injection and the disappearance of Green Deal and CBAM costs.

• Industrial re-migration to Europe — without a single hectare of European farmland being sacrificed. Production lies where the plant grows; the benefit lies where the buyer lives.

• A new European-equatorial strategic axis as an alternative to dependence on Russian gas and American LNG.

• Brussels as a net enricher, provided it has the courage to abolish the Green Deal and CBAM in favour of a mechanism that meets the same climate objective at a sixth of the price.

• The industrial layer in its own hands: under an active EU industrial strategy, 840,000 jobs and €65 billion in annual turnover remain within the Union — BiCRS machines, ethanol plants, micro-CHP units, bioplastic production. Under the default course this shifts to China, as happened with solar panels and wind turbines.

• The plastic doctrine as a third climate pillar: 228 Mt of CO₂ per year (7.6% of EU emissions) sequestered in bioplastic storage, 60 TWh of recycling energy freed up, 120,000 jobs added, and 19.2 Gt of storage capacity in German lignite pits — a buffer for six years of EU emissions.

The summed Brussels outcome

When all the reforms are counted together, without double-counting, the Brussels Consequences Map BiCRS course yields the following profile:

Net difference, citizen/business 2030: +23 to +106% income-equivalent

CO₂ removal via BiCRS injection: 2.8 Gt/yr world; €112 bn EU cost

CO₂ sequestration via bioplastic storage: 228 Mt/yr EU (7.6% of emissions)

Recycling energy freed up: 60 TWh/yr (= Belgium's annual use)

Strategic storage capacity, German pits: 19.2 Gt CO₂ = 6.4 yrs EU emissions

EU jobs under an active industrial strategy: 840k BiCRS+ethanol+CHP + 120k bioplastic = 960k

EU production turnover within the Union: €65 bn/yr BiCRS chain + €8 bn bioplastic

Time frame to first implementation: 12-24 month decision window

A million jobs, a fifth of European emissions removed or sequestered, a new strategic axis with the equatorial band, and an industrial layer that stays in Europe rather than shifting to China. None of these outcomes requires new technology or new treaties — they require only the Brussels decision to replace the Green Deal and CBAM with an instrument that meets the same climate objective at a sixth of the price, plus the plastic doctrine that shifts petrochemistry from extraction to storage.

"The question for the European voter is not whether climate policy is needed. It is whether Europe chooses a climate policy that destroys its prosperity base, or a climate policy that multiplies its prosperity base. The difference between those two courses is measured in hundreds of billions of euros per year. The technology for the second course is ready — and the plant grows on the equator, not in Brussels."

— Brussels Consequences Map BiCRS version, closing thought

Methodology and sources

The model uses the same three-step method as the original Brussels Consequences Map (direct wallet, macro effect, cascade), with the following changes in the matrix columns:

• Green Deal package (cumulative) — visible in the original matrix; abolished under BiCRS implementation

• CBAM + carbon border adjustment — visible in the original matrix; abolished under BiCRS implementation

• BiCRS replacement column (net difference) — new, added before Nova Democratia. Calculation: BiCRS benefit minus Green Deal cost minus CBAM cost.

• Bioethanol track — a separate track with its own hectares, its own plants and its own contract model; not included in this piece's BiCRS benefit calculation

Scientific underpinning of the calculation:

• Anoxic biomass conservation: natural peat-formation studies show 80-95% carbon retention over centuries under oxygen-free conditions (Limpens et al., Biogeosciences 2008; Page et al., Nature 2011 on tropical peat). Liquefied biomass via cell disruption distributes more evenly than solid biomass, so that the anoxic environment becomes homogeneous more quickly and oxidative edge zones are minimised.

• Biomass carbon fractions of 46-48% in plant dry matter (US Department of Energy BETO 2019).

• Root mass 25% of plant CO₂, permanently in soil at 0-2 m depth (Jackson et al., Nature 2017 on soil-carbon distribution).

• Methane emission of tropical rainforest: Pangala et al., Nature 2017 ('Large emissions from floodplain trees close the Amazon methane budget') estimate ≈20 Tg CH₄/year from Amazon tree trunks alone, alongside comparable emissions from tropical peatlands in the Congo cuvette and Indonesia (Dargie et al., Nature 2017; Page et al., Nature 2011). Methane GWP values: IPCC AR6 WG1 Chapter 7 (2021): GWP-100 = 27-30, GWP-20 = 81-83.

• Tropical rainforest net-carbon balance: Pan et al., Science 2011 ('A Large and Persistent Carbon Sink in the World's Forests') for the uptake side; Brienen et al., Nature 2015 on the weakening of the Amazon sink (-30% decline 1990-2010); Mitchard, Nature 2018 for revised tropical sink estimates.

• Bioethanol from lignocellulose 197-470 L/tonne biomass, production cost approaching €0.20/litre at scale (NREL Process Design 2015; IEA Bioenergy Task 39 cost-reduction studies 2020).

• Equatorial biomass yields 250-600 tonnes fresh/ha/year for tropical C4 grasses (Pennisetum, Miscanthus tropicalis, Napier) under optimal conditions (FAO Tropical Biomass Production Survey 2019).

Sources for the Brussels status quo 2026:

• EU ETS price June 2026: €78/tonne (Investing.com ICE EUA futures)

• CBAM implementation 2026: €82/tonne effective import tariff (European Commission CBAM monitoring)

• Fit-for-55 total implementation cost 4-6% of EU GDP (DG CLIMA Impact Assessment 2024)

The Excel model with all 20 BiCRS scenario functions and the difference calculation will be made available on eu-bicrs.openvizier.org when the platform goes live.

Limitation: as in all Consequences Maps, the matrix shows, per column, the cumulative effect under the assumption that that mechanism is dominant. In practice a household experiences the summed effect with overlap between mechanisms. The matrix is a map of potential sources of influence, not a guaranteed total.

WRITTEN BY JACOBUS VAN MERKSTEIJN WITH EDITORIAL AI SUPPORT

HET OPEN VIZIER — OPENVIZIER.ORG

DE GEVOLGENKAART-REEKS — GEVOLGENKAART.NL • KONSEQUENZKARTE.DE • KONSEGWENZI.MT • EU.GEVOLGENKAART.NL • TRUMP-SPIEGEL.OPENVIZIER.ORG • EU-BICRS.OPENVIZIER.ORG

JUNE 2026

GESCHREVEN DOOR JACOBUS VAN MERKSTEIJN MET REDACTIONELE AI-ONDERSTEUNING

HET OPEN VIZIER · OPENVIZIER.ORG · JUNI 2026