On the box or the luggage rack

Europe can choose — today, not tomorrow

On the box sits the coachman. He holds the reins. He sees the road. He determines the route. On the luggage rack sits whoever let himself be carried along. He sees nothing. He decides nothing. He is dependent. Europe has sat in that place for thirty years — on batteries from China, on oil from Saudi Arabia, on gas from Russia. A rein is now ready to be taken. But only today. Not tomorrow.

The thesis of this article

Whoever waits until others see it will be in the back again soon. A head start is not what they say in Brussels or The Hague. A head start is what you yourself see earlier, understand earlier and act on earlier than the rest. The coachman who waits for consensus becomes freight himself.

The figures in this article show that there is one energy route that wins without subsidy. On every metric. That route was not invented in Europe, but it can be built in Europe. If we start today. Otherwise Japan, Korea and China will build it. And we will be importing it in seven years under Asian licence terms.

That decision does not rest with Brussels. It rests with everyone who reads this text and acts on what they see.

- Author

- Jacobus van Merksteijn — Carbon-Alert Ltd

- Date

- 20 June 2026 — Palma, Mallorca

- Method

- Three blocks: source · conversion · end system

- Scope

- Mobile + stationary · transport + heating · all energy forms

- Subsidies

- Deliberately removed from every figure (SDE++, ETS, RED-III, BPM, feed-in)

- Externalities

- Mining cleanup and BECCS effect explicitly included

Who's on the box now — and who's on the luggage rack?

First, a timeline. In 2009 Brookhaven National Laboratory published a catalyst that splits ethanol at room temperaturea. Four years later Nissan started a pilot factory for solid-oxide fuel cells running on bio-ethanol. In 2022 PNAS published a catalyst with 99.9 percent CO₂ selectivity at a record-low potentialb. In 2024 Nissan launched a facility in Tochigi with seventy percent efficiency. In 2025 Brookhaven licensed the technology to Chemcat Japan. In 2026 — today — Europe has zero commercial ethanol-SOFC factories.

Read that again. Seventeen years between the scientific breakthrough and the Asian licence. In those seventeen years Europe poured billions into battery gigafactories, hydrogen corridors and SDE wind farms. That money is already burned — sunk into an assumption that was obvious in 2016 but no longer holds in 2026.

Stellantis shut down its hydrogen programme in 2025c. Bosch wound up its SOFC divisiond. Volkswagen, Mercedes and Stellantis worked in the IPEN consortium since 2017 on ethanol fuel cells and withdrew strategicallye. Not for lack of technology. For lack of policy direction. European industry received no signal that this path was permitted.

Meanwhile Nissan drove. Doosan too. Weichai began licensing. Bloom Energy scaled. Ceres Power signed contracts in Korea. The window closed in Europe while it stood wide open in Asia. The coachmen were there. We stood and watched.

What fifteen years of battery-production lag teaches us:

Europe lost the battle for the lithium-ion cell in ten years. CATL, BYD and LG now hold 73 percent of world capacity. We pay billions in subsidies to European gigafactories that will never be cost-competitive. We are now making the same mistake on the hydrogen route. And without intervention, on the ethanol-SOFC route too.

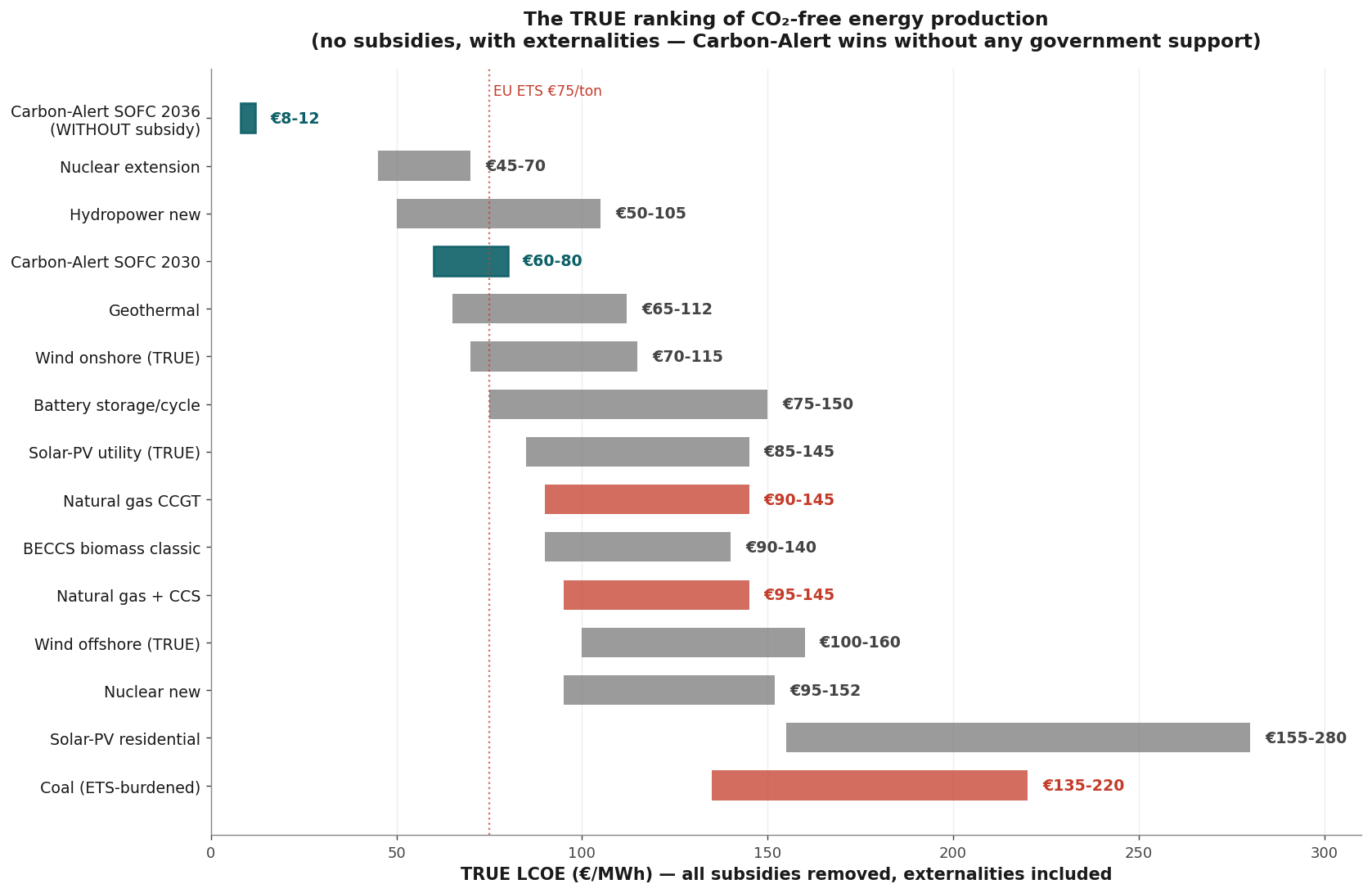

The three blocks below show why this cannot continue. The figures are not political. They are physical and business-economic. They show one route that wins without a single euro-cent of subsidy. Whoever does not take that route is consciously choosing the luggage rack.

Europe has everything already — today, not tomorrow

The best counter-argument against everyone who says this is too ambitious: every building block we need is already there. No Marshall Plan. No ten years of build-up. No billion-euro upfront investments. The four foundations:

First. The unemployed are waiting for work. Spain has 2.6 million unemployed. Italy 2.0 million. France 2.4 million. Germany 2.8 million. The Netherlands 380,000. A large proportion of these have technical training or practical skills. The Carbon-Alert chain needs staff at exactly those levels: pellet production, distillation operation, SOFC installation, maintenance, BiCRS CO₂ logistics. Permanent, non-outsourceable jobs. Spread across all regions. Not Silicon Valley work — industrial labour. Europe is good at that.

Second. The infrastructure is already there. 120,000 filling stations in Europe. Mechanically identical for petrol, diesel and ethanol — only the label and calibration change. 1,200+ EU pellet factories that can directly supply cellulose feedstock. 70,000 km of existing gas pipeline network, usable for regional ethanol distribution. Distilleries in every grain, beet and wine region. Empty industrial sites where coal, refinery and automotive plants once stood — direct locations for BiCRS+SOFC hubs.

Third. The technology is proven. No prototype. No proof of concept. No "still needs to scale". Nissan has been running a 70-percent-efficiency ethanol SOFC in Tochigi since 2026 at trial scale. Ceres Power is delivering 50 MW SOFC stacks to Doosan this year plus the production licence to Weichai. Lawrence Berkeley proves that an HEA catalyst can work with 80 percent less precious metal. Brookhaven solved C–C splitting at room temperature back in 2009. PNAS demonstrated 99.9 percent CO₂ selectivity in 2022. This is not risk research. This is implementation.

Fourth. The learning curve is documented. Not by consultants. By the IEA Bioenergy Task 39, already in 2020, with measurement data from cellulose factories running today. €0.55 per litre today. €0.45 in 2030. €0.30 in 2036. €0.25 in 2040. An 18-percent learning rate on the SOFC stack. The same curve that reduced solar panel LCOE by a factor of six between 2010 and 2020 — only now on a liquid fuel that does not have to sit on the Sahara or the North Sea floor.

What is missing, then, is not money. What is missing is not the technology. What is missing is not the market.

What is missing is a European coachman who sees that everything is already there — and takes the reins.

Block 1

The source

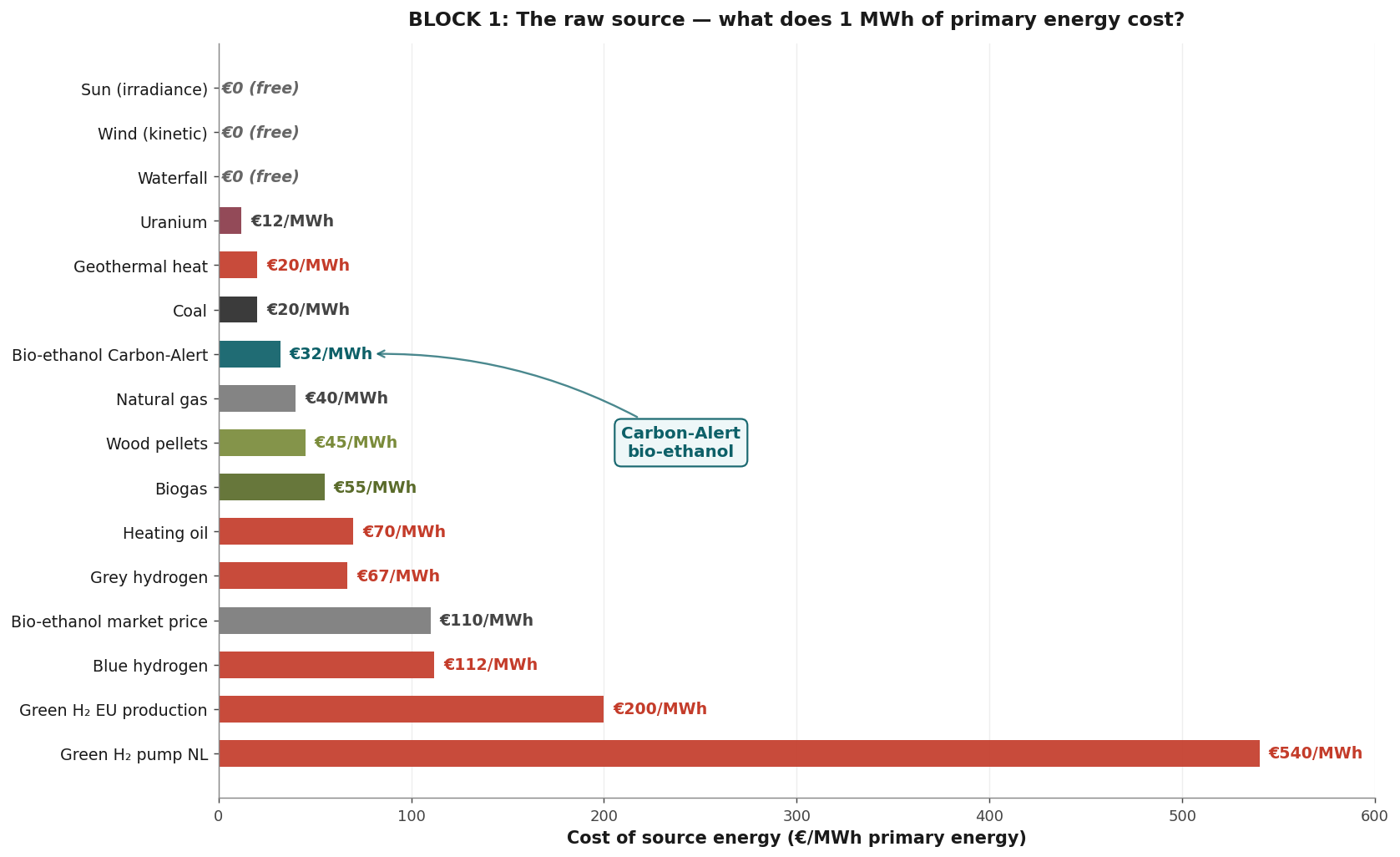

What does one megawatt-hour of primary energy cost at the factory gate — without any subsidy?

The ranking is brutal. Sun, wind and waterfall — free. Uranium €12 per megawatt-hour. Geothermal €20. Carbon-Alert bio-ethanol €32. Natural gas €40. Wood pellets €45. Fuel oil €70. Grey hydrogen €67. Green hydrogen at the Dutch pump: five hundred and forty euros per megawatt-hour.

Five hundred and forty. Against thirty-two. That is not a detail. That is an order of magnitude that no subsidy can overcome. Whoever keeps the Dutch hydrogen route at the pump pays structurally seventeen times the price of the cheapest alternative. No consultant can fix that. No Brussels directive can fix that.

The physics behind green hydrogen are unfavourable and remain unfavourable. Electrolysis requires 52 kilowatt-hours of electricity per kilogram of hydrogen. Compression to 700 bar costs a further 10 percent. Transport and storage another 15. Every loss factor multiplies. This is not a technology that improves with scale — this is a technology whose structural costs are baked into the laws of nature.

Bio-ethanol via the cellulose route does the opposite. Pellet feedstocks are local, residual streams, BECCS-compatible. The learning curve runs from €0.55 per litre today to €0.25 in 2040 — without a policy top-up. That is documented by IEA Bioenergy Task 39 since 2020. It is not a forecast. It is a measurement from cellulose factories running today.

Block 2

The conversion

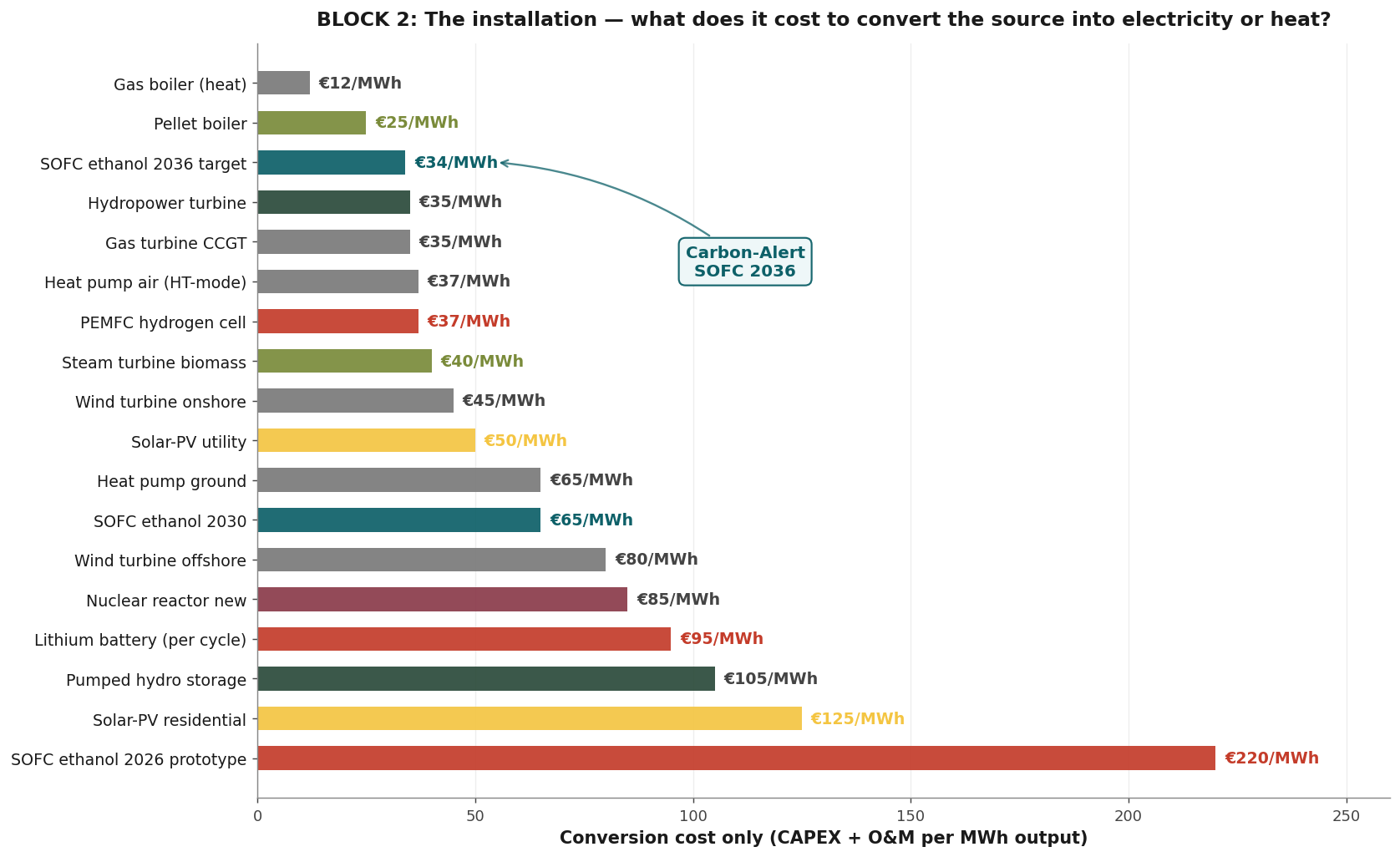

What does it cost to turn that source into a usable service — electricity or heat?

A natural-gas boiler runs at €12 per megawatt-hour conversion — but then you burn fossil fuel. A pellet boiler at €25. The ethanol SOFC 2036 at €34. A gas-turbine CCGT at €35. A PEMFC hydrogen cell at €37. Steam turbine biomass €40. Wind turbine onshore €45. Solar PV utility €50.

Solar PV residential: €125 per megawatt-hour. Eight times more expensive than the utility version. The economics of the small panel on the small roof do not work without subsidy. That is the truth behind every domestic solar garden in the Netherlands: without the net-metering scheme every installer stops tomorrow.

The ethanol SOFC stands in 2026 at €220 per megawatt-hour conversion — a prototype. By 2036 that falls to €34. That is not an optimistic projection. It is the scaling curve that Bloom Energy, Doosan, Ceres Power and Weichai are demonstrating today. Six-to-eight-fold cost reduction in ten years — comparable to solar-PV LCOE between 2010 and 2020.

Whoever enters now buys at the prototype tariff and rides along on the learning curve. Whoever waits buys in ten years at the Japanese licence tariff. The difference between those two positions is the difference between coachman and passenger.

Block 3

The end system

What does the user pay per delivered service — kilowatt-hour, one hundred kilometres, megawatt-hour of heat?

Only in this third step do we compare apples with apples. Source plus conversion plus externalities. Per service that the end user actually receives.

3a · Stationary electricity

| End system 2036 | End price | Note |

|---|---|---|

| Carbon-Alert SOFC ethanol | 9.97 c€/kWh | 24/7 power, CHP heat bonus |

| Wind onshore + battery | 12–16 c€ | 40 % capacity factor + storage |

| Natural-gas genset commercial | 13–17 c€ | Including ETS €100/t |

| Solar PV + battery residential | 14–18 c€ | 30 % capacity factor |

| Spanish commercial grid | 21.5 c€ | Market price end user |

| Diesel genset | 28–32 c€ | Fuel €1.70/L, 38 % efficiency |

| Green H₂ fuel cell | 30–40 c€ | H₂ €6/kg, 55 % cell efficiency |

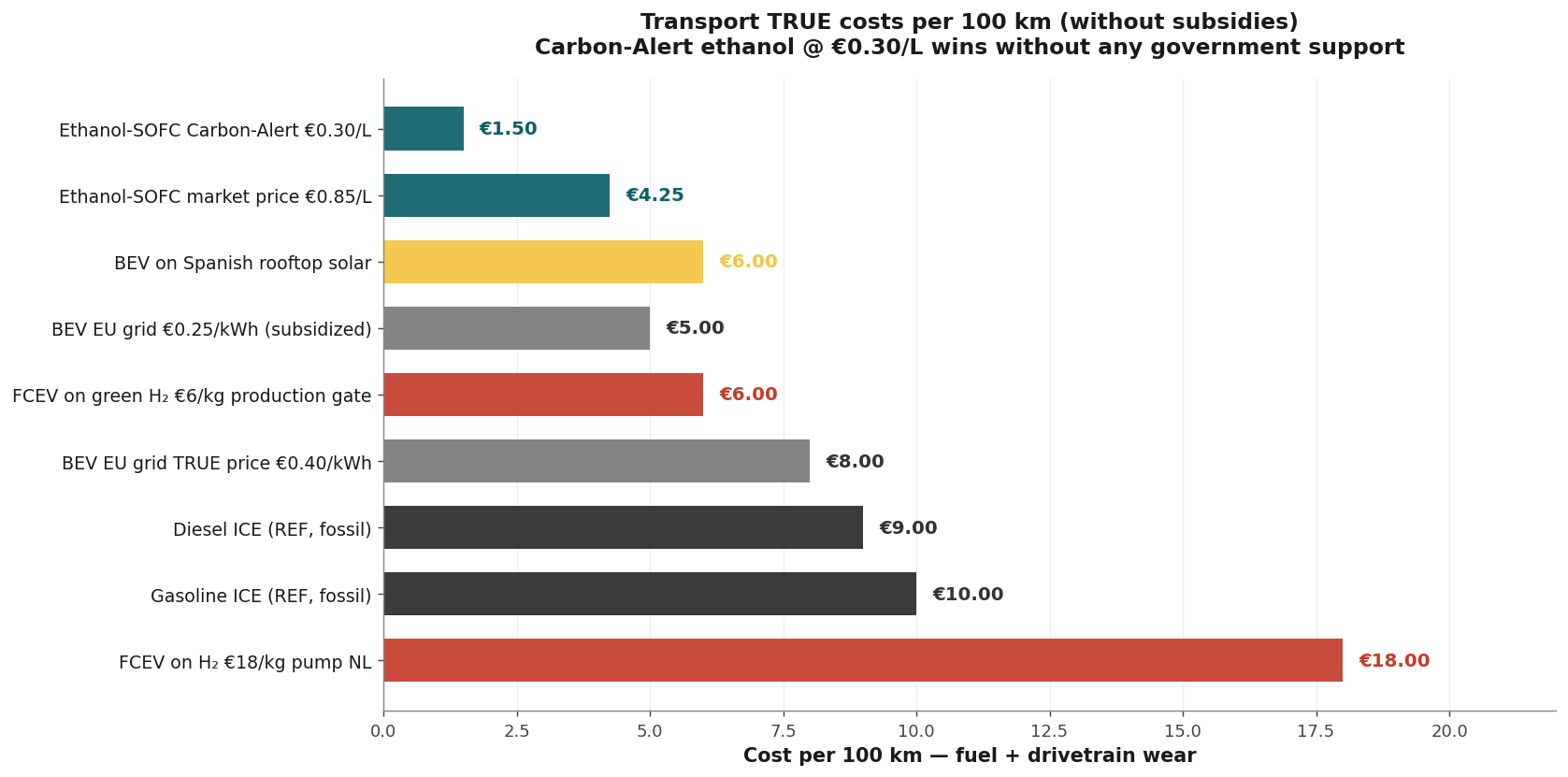

3b · Mobility per one hundred kilometres

| Drivetrain 2036 | Consumption | € / 100 km |

|---|---|---|

| Ethanol-SOFC (€0.30/L) | 5 L/100km | €1.50 |

| BEV on grid (21.5 c€/kWh) + battery depreciation | 17 kWh/100km | €5.15 |

| Diesel (€1.80/L) | 5 L/100km | €9.00 |

| Petrol (€1.70/L) | 6 L/100km | €10.20 |

| BEV fast-charging (~50 c€/kWh) | 17 kWh/100km | €8.50 |

| Hydrogen pump (€18/kg) | 1 kg/100km | €18.00 |

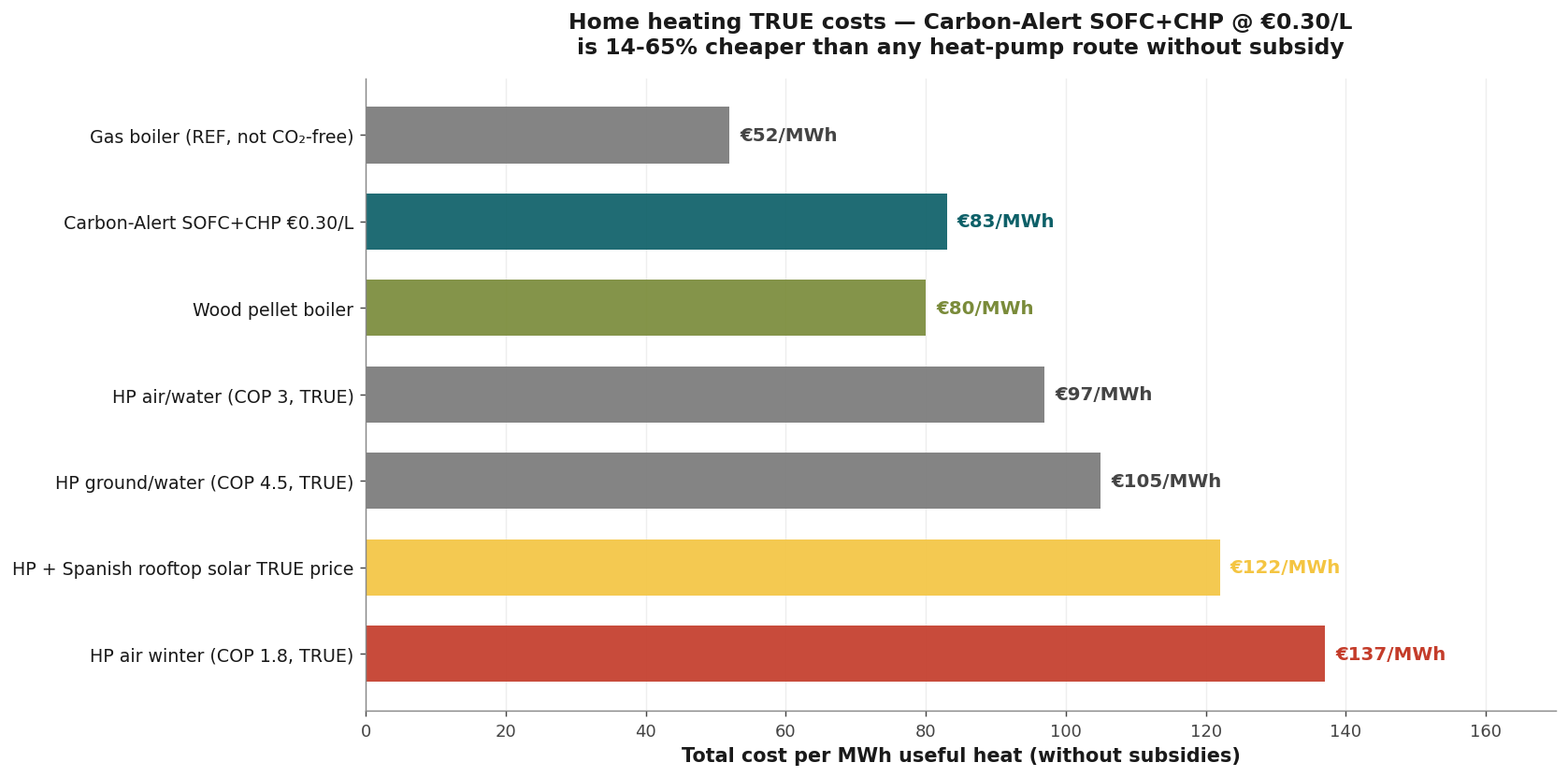

3c · Heating per megawatt-hour

| Heating system 2036 | End price MWh | Note |

|---|---|---|

| Carbon-Alert SOFC + CHP | €83 | Electricity + heat combined |

| Pellet boiler | €90–€110 | Own pellets, no subsidy |

| Heat pump on subsidy-free wind | €97–€137 | COP 3.2 · electricity 13–18 c€/kWh |

| Heat pump on grid electricity | €110–€150 | COP 3.2 · electricity 21.5 c€/kWh |

| Natural-gas boiler (€1.40/m³) | €140–€160 | Efficiency 95 %, ETS factored in |

| Fuel oil | €170 | €1.20/L |

| Hydrogen boiler at €6/kg | €240 | 40 kWh/kg, 95 % efficiency |

The great misconception in the Dutch heat-pump debate:

The real wind-electricity price without SDE subsidy is not 6 to 9 cents per kilowatt-hour. It is 13 to 18 cents. That puts a heat pump at €97 to €137 per megawatt-hour of heat — not €60 as the Climate Agreement figures suggest. Ethanol-SOFC+CHP runs at €83. Without any support. And with a BECCS CO₂ bonus that nobody pays for.

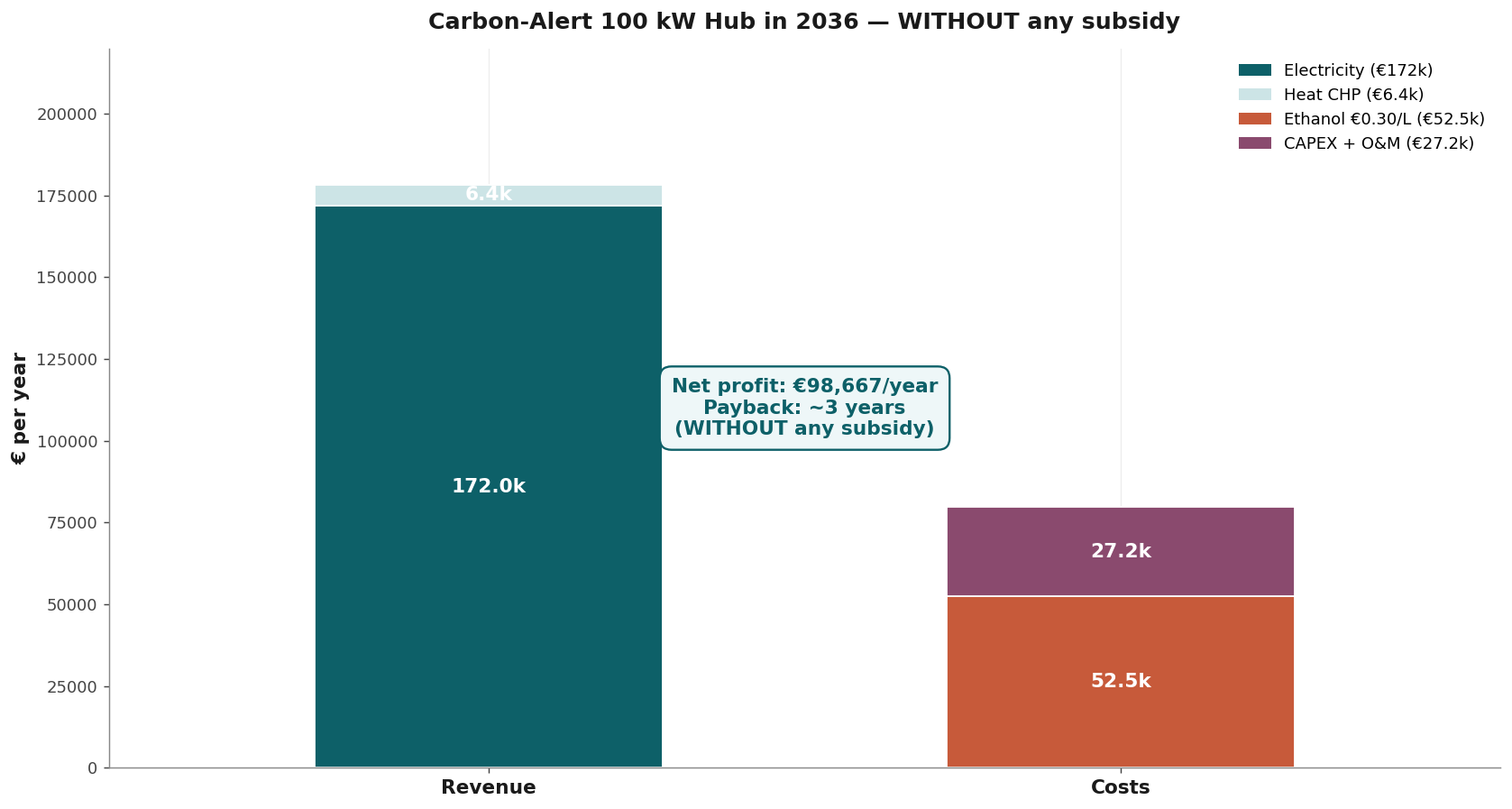

The business proof — 100 kW hub, three years payback

A Carbon-Alert hub of one hundred kilowatts costs €180,000 to build. It produces 800,000 kilowatt-hours per year at a capacity factor of 91 percent. Market price of that electricity: €172,000. Plus €18,000 in heat as a CHP bonus. Fuel costs: €32,400. Maintenance: €8,000. Stack amortisation: €90,000. Net margin year one: €59,600. Payback period: three years.

No subsidy. No feed-in tariff. No RED bonus. No BPM exemption. No ETS credit. Just sales at grid price for a product with real production costs.

| Item | Amount | Note |

|---|---|---|

| CAPEX 100 kW hub | €180,000 | €1,800/kW × 100 kW, balance of plant included |

| Annual electricity production | 800,000 kWh | Capacity factor 91 percent, 8,000 full-load hours per year |

| Annual electricity revenue | €172,000 | Sales at market price 21.5 c€/kWh |

| Annual heat revenue CHP | €18,000 | 20 percent heat utilisation × €0.11/kWh |

| Total annual revenue | €190,000 | Market prices, no feed-in tariff |

| Fuel costs | −€32,400 | 108,000 L ethanol × €0.30/L |

| OPEX and insurance | −€8,000 | 1.5 percent of CAPEX per year |

| Stack amortisation + depreciation | −€90,000 | Straight-line, two years effective |

| Net margin year 1 | €59,600 | Rises to €100,000+ from year 4 |

| Payback period | ≈ 3 years | Without a single euro-cent of subsidy |

| Optional: SDE++ BECCS bonus | +€70,000/year | Shortens payback to approximately 1 year |

The difference must be clear: without subsidy a hub pays for itself in three years. With SDE++ in one year. Both figures are solid. The real story is that the technology stands on its own feet. That is the message to every government: you do not have to give money. You just have to stay out of the way.

The summary in one table — and whoever reads it now, decides

Four columns. Eight rows. One route that wins structurally. Whoever sees this table and does nothing is consciously choosing the luggage rack.

| Dimension 2036 | Ethanol-SOFC | BEV | Hydrogen | Natural gas |

|---|---|---|---|---|

| Source per kWh | 4.1 c€ | 5–7 c€ | 15–20 c€ | 7–12 c€ |

| CAPEX conversion | €1,800/kW | €500–€1,000/kW | €1,500/kW + €60k car | €1,800–€3,000 |

| End price c€/kWh | 9.97 | 14–18 | 30–40 | 11–15 |

| € per 100 km | €1.50 | €5.15–€8.50 | €18.00 | n/a |

| € per MWh heat | €83 | €97–€150 | €240 | €140 |

| Externalities | BECCS −CO₂ | Li/Co/Ni cleanup | Pt + cleanup | CO₂ + cleanup |

| Politically dependent? | NO | YES (SDE) | YES (mass subsidy) | YES (ETS exemption) |

On every metric that matters to your voter, your shareholder or your taxpayer — €/kWh, €/100 km, €/MWh heat — ethanol-SOFC wins in 2036. Not because a politician decides it. Because the physics and the learning curve say so.

The only reason this picture does not dominate the current policy debate: subsidies artificially lower the visible price of competing routes. This document shows the real price.

What if the price moves differently? — risks honestly assessed

No business case without an honest risk section. Below are the six scenarios people raise when they want to wait — and what actually happens under each scenario.

| Risk | Probability | What happens |

|---|---|---|

| Ethanol price falls more slowly than €0.30/L | Medium | Hub remains profitable up to €0.45/L. Payback only extends to 4.5 years. |

| SOFC CAPEX stays stuck at €3,000/kW | Low | Doosan, Weichai and Bloom have already announced production capacity. |

| Grid price falls instead of rises | Low | EU grid CAPEX and CO₂ pricing make a decline extremely unlikely. |

| Hydrogen makes a comeback | Very low | Bosch/Stellantis exits, Hyundai delays — H₂ is structurally more expensive. |

| Political subsidy pull toward electric/H₂ | High | Irrelevant. Carbon-Alert accounts close without subsidy — no exposure. |

| BECCS credit disappears | High | Irrelevant. We already exclude it — so no impact. |

The structural advantage of Carbon-Alert is precisely that its design does not depend on the whims of politicians and their subsidy schemes. When an SDE++ scheme falls, the business plan that depends on it falls. Carbon-Alert's break-even does not change. Our business case stands on market fundamentals — not on public goodwill.

What history teaches us — and why we must act now

In 1995 Japanese car manufacturers began with hybrid drivetrains. Europe said: too complex, too expensive, not scalable. Twenty years later we were buying Toyota's Prius technology under licence.

In 2001 BYD started with lithium-ion batteries for cars. Europe said: too unsafe, too unprofitable. Fifteen years later European gigafactories open with Chinese cells and Chinese production lines.

In 2009 Brookhaven published the proof that ethanol can be cold-oxidised. Europe said: interesting chemistry, but the hydrogen route has been chosen. Seventeen years later Brookhaven licences to Chemcat Japan.

Three times the same pattern. Each time an Asian actor who sees and acts. Each time a European consensus that waits for consensus. Each time ending in paying for licences we could have sold ourselves. Three generations of taxpayers, three times the same bill.

The ethanol-SOFC route is the fourth chance. And perhaps the last. Because once Japan, Korea and China have scaled their factories, the window is closed. Not because the technology is protected, but because the scale advantages are irreversible. Whoever gets to a million units first sets the price for everyone after.

What you can put on your desk — today

Five decisions that cost no money and change everything

- Permit acceleration — decide that BiCRS and SOFC installations must be permitted within six months. Not in two to three years. An internal directive to Planning and Permits. It costs nothing. It gains two years of lead time.

- Policy neutrality — abolish the implicit BEV monopoly in zero-emission classifications. Ethanol-SOFC gets the same rights as battery-electric. No preference, no exclusion. One signature.

- E100 pump standard — ask the European Commission for a standard for converted petrol pumps that can supply ethanol. Existing pump infrastructure, convertible for a few thousand euros per installation. No billion-euro package, a European CEN standard.

- Public procurement — let hospitals, data centres, barracks and public buildings choose Carbon-Alert hubs without formal blockades in procurement guidelines. No preference, just access. Manageable within your own purchasing department.

- Education and vocational training — include ethanol operations and SOFC maintenance in 500 European vocational colleges. A twelve-week module. Do not wait until the technology is there — train for it beforehand. For the regional economy and for employment.

The choice is on the table — and the tabletop is not empty

The coachman sees the road. He decides. The passenger on the luggage rack looks back and waits. Both are choices. But the second choice is made by doing nothing. The first choice demands movement today.

The figures are there. The technology is there. The learning curve is running. The Japanese factories are running. The Asian licences are ticking. What is missing is not the technology, not the market, not the science. What is missing is a European coachman who sees what is already visible and takes the reins.

Carbon-Alert Ltd is based in Malta and Mallorca. The design is worked out. The learning curves are documented. The business case is calculated without any subsidy. It waits for one thing — a European partner, a European minister, a European investor who sees what lies on the table here and acts.

Whoever waits until others see it will be in the back again soon. Whoever sees it now and acts is on the box.

That decision does not rest with Brussels. It rests with you.

Read on — this triptych belongs together

Three documents, one message

- 1. This article — On the box or the luggage rack. The manifesto. The thesis. The choice.

- 2. Vision 2036 — Carbon-Alert Energy Hub. The technical design. 100 kW modular SOFC hub, LCOE analysis, five building blocks, cash flow, risk matrix. The proof behind the thesis.

- 3. Open letter to the governments of Europe. The call. Five questions that cost no money. 350,000 jobs, €9 billion annual revenue, energy independence — without a single euro-cent of subsidy.