The thirty cents that flip Europe

Electric. Hydrogen. Fossil. Ethanol. Heat pump. Compare them all, for transport and heating, without a single eurocent of subsidy. One route wins. You don't hear about it in Westminster, Berlin, or Brussels.

- Author

- Jacobus van Merksteijn

- Date

- 20 June 2026 — Palma, Mallorca

- Section

- Research & analysis

- Method

- All prices calculated without any subsidy (SDE++, ETS credit, RED bonus)

- Sources

- Fourteen scientific and industry sources — see footnotes and appendix

The cold breakthrough no one explains

First this. Ethanol oxidises cold. No flame. No turbine. No piston. A static cell, room temperature to eighty degrees, and current flows out. That is not science fiction. It is called a Direct Ethanol Fuel Cell — a DEFC. And performance has silently broken through the ceiling over the past few years.

The theoretical upper limit: cell voltage 1.14 volts, Gibbs efficiency 97 percent. Full oxidation to CO₂ yields twelve electrons per ethanol molecule. Break the C–C bond at low temperature and those twelve are unlocked. That is exactly what has been achieved.

Room temperature. Power density at 25 °C:

140 mW/cm² with commercial alkaline membranes and non-precious-metal catalyst · 438 mW/cm² with Pd/Co@N-C, stable for over a thousand hours · 570 mW/cm² with nitrogen-rich palladium, stable for 5,900 hours · 1,009 mW/cm² with a new acid-stable Pd catalyst.

One square centimetre. One watt. At room temperature. Compare that with a lithium-ion cell that heats under load, or a hydrogen PEM that achieves seventy percent efficiency only when the membrane stays moist. Here is a liquid you pour into a bottle, a catalyst that does not need to boil, and a continuous current.

Splitting the C–C bond at low temperature was the bottleneck for decades. Brookhaven National Laboratory solved it with platinum-rhodium on tin dioxide — a ternary system that breaks C–C at room temperaturea. PNAS published in 2022 a single-atom Rh on Pt nanocube achieving 99.9 percent CO₂ selectivity at a record-low potential of 0.35 Vb. The science is complete. What is missing is scale-up.

What this means for Europe: a static, silent, room-temperature energy source running on liquid fuel exists. No 700-bar tank. No cryogenic cylinder. No rare earths. No Congolese cobalt. A catalyst with palladium or platinum-rhodium in micrograms, a membrane, and a bottle of ethanol. Done.

Full oxidation is not yet perfect. Many DEFCs stop at acetic acid — four electrons instead of twelve. Faradaic efficiency in practical cells therefore remains 37 to 54 percent. But the catalysts that do achieve full oxidation already exist — they are being demonstrated today in laboratories at Brookhaven, Lawrence Berkeley, Fraunhofer, and UCF. This is a manufacturing question, not a science question.

Three numbers to remember:

· 1.14 V theoretical cell voltage

· 97 % Gibbs efficiency at full oxidation

· 1 W/cm² achievable power density at room temperature, today

This is the engine beneath everything that follows. Without cold oxidation, no 9.97 cents per kilowatt-hour. Without cold oxidation, no €1.50 per hundred kilometres. Without cold oxidation, no jobs created in Brabant, Bavaria, and Catalonia. The entire story rests on this one catalytic leap.

And yet you hear nothing about it in The Hague, Berlin, or Brussels. That is what the rest of this article is about.

The silence around a cheaper alternative

The European energy debate turns on three words: electric, battery, hydrogen. Propose anything else and you are told it does not scale. Not clean. Not policy-friendly. Behind the scenes, something is changing.

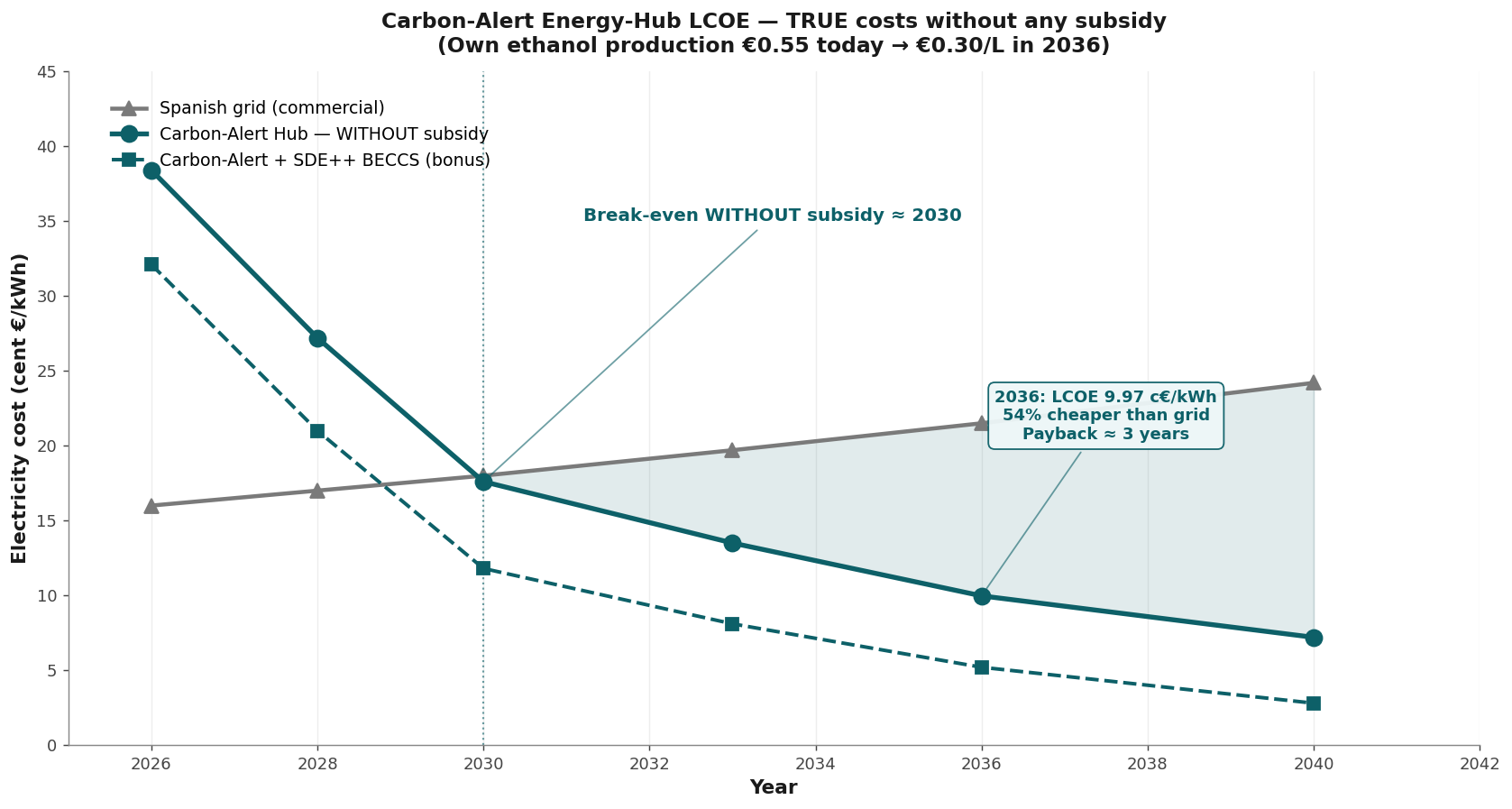

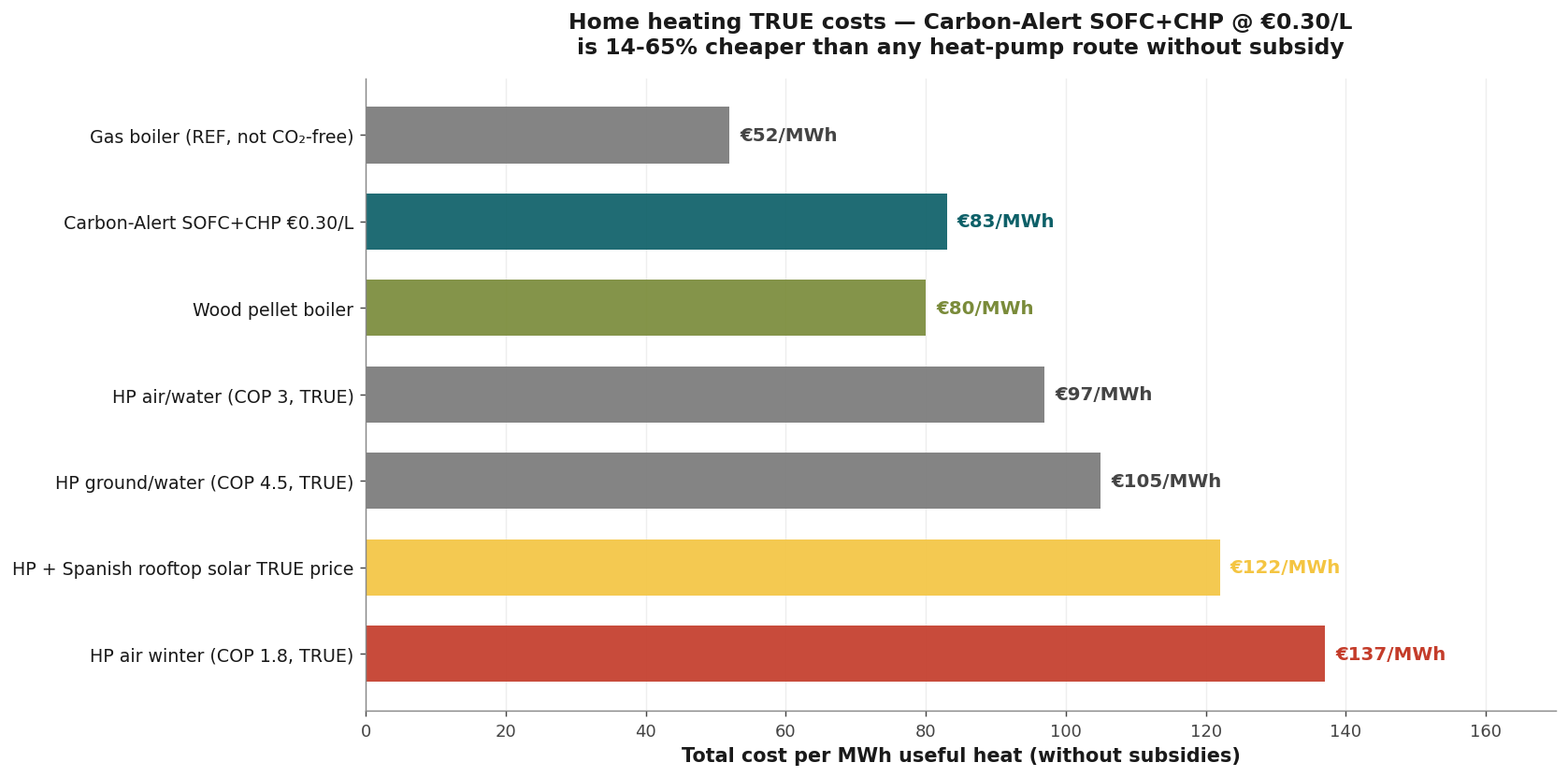

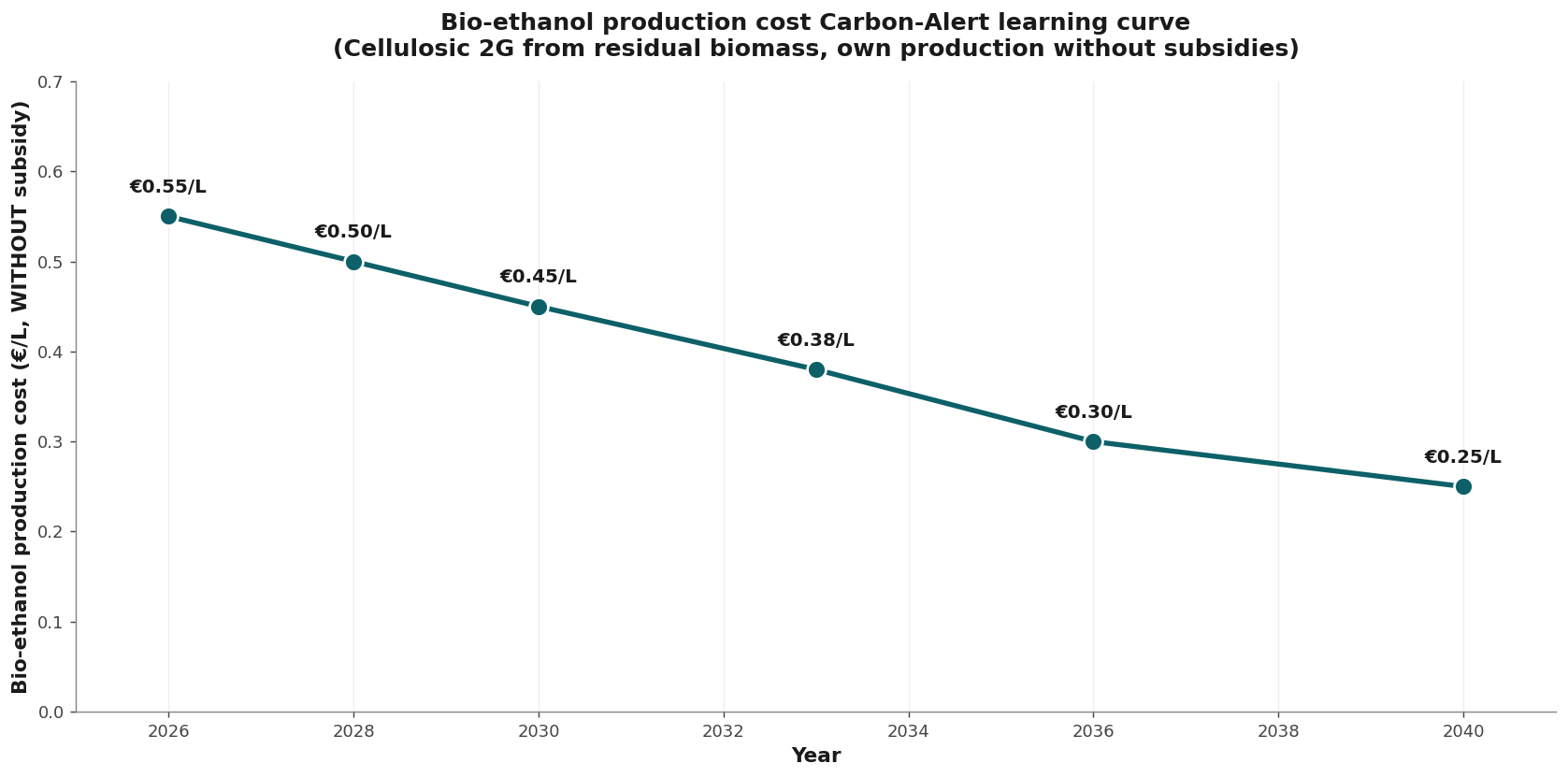

In Tochigi, Japan, a Nissan installation has been running since 2026, converting bio-ethanol into electricity at seventy percent efficiency1. No European automotive or energy technology matches that. Meanwhile the production cost of cellulose-ethanol is steadily falling to thirty cents per litre in 2036. No subsidy required.

That second number is the core. Thirty cents per litre is not a slogan and not PR. It is the projection of the learning curve that IEA Bioenergy Task 392 has been documenting since 2020. Economies of scale. Better fermentation. Pellet feedstocks. BECCS integration. Seven to nine percent cost reduction per year. €0.55 today. €0.45 in 2030. €0.30 in 2036. No subsidy needed.

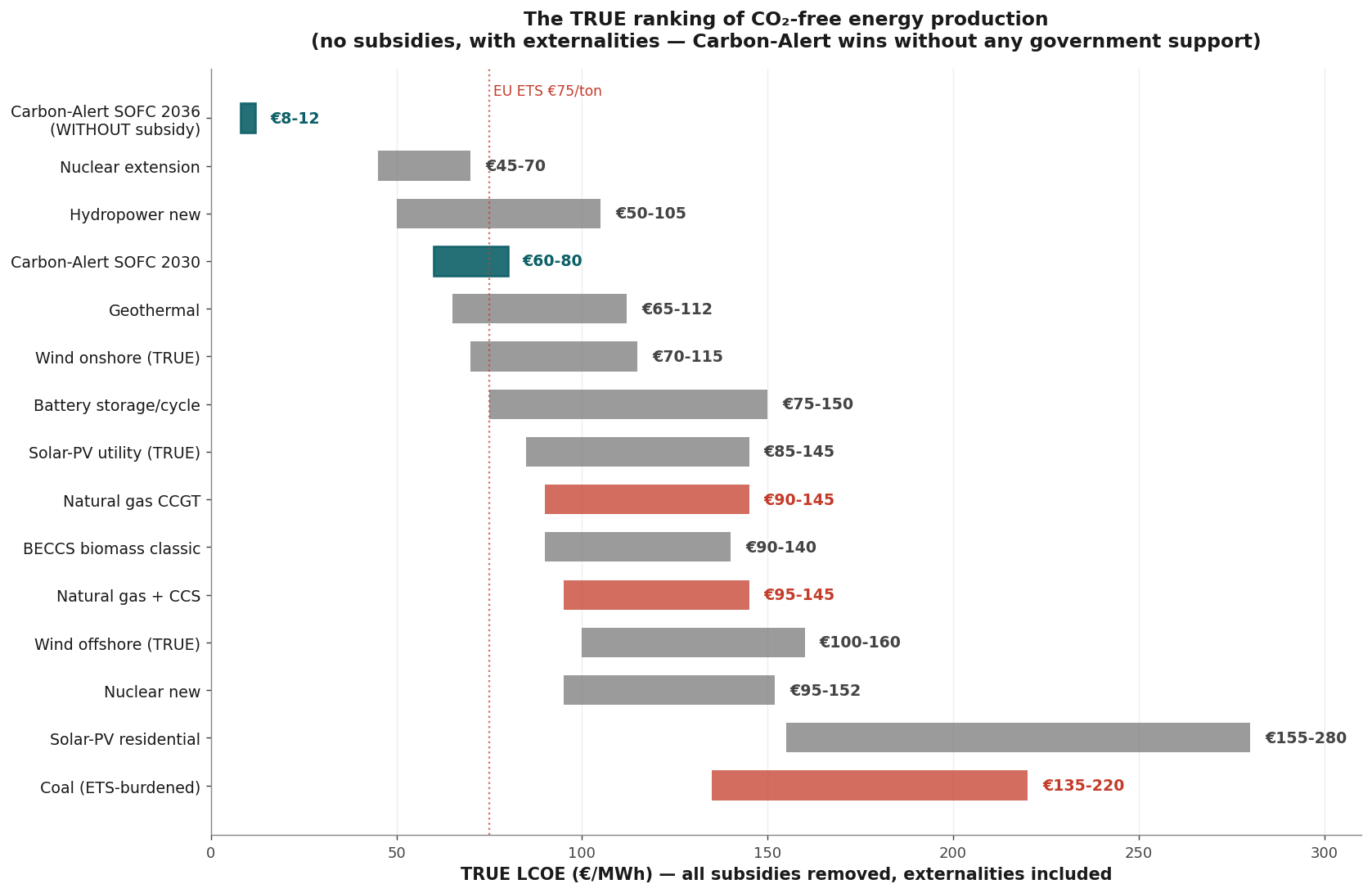

All energy side by side — without subsidy

Most European policy tables compare apples with oranges. Electric vehicles include purchase subsidies and registration-tax exemptions. Ethanol vehicles are measured at the gross pump price including excise duty. Wind power is priced at the subsidised rate. Ethanol-SOFC at the gross production cost.

This article sets everything to zero. No subsidies. No ETS credits. No feed-in tariffs. No RED bonuses. Only what stands on its own technical and economic feet.

The comparison — all prices without subsidy, 2036:

Carbon-Alert ethanol-SOFC 9.97 c€/kWh · Spanish grid 21.5 c€/kWh · Green hydrogen fuel cell 30–40 c€/kWh · Diesel genset 28–32 c€/kWh · BEV on rapid charge 50 c€/kWh.

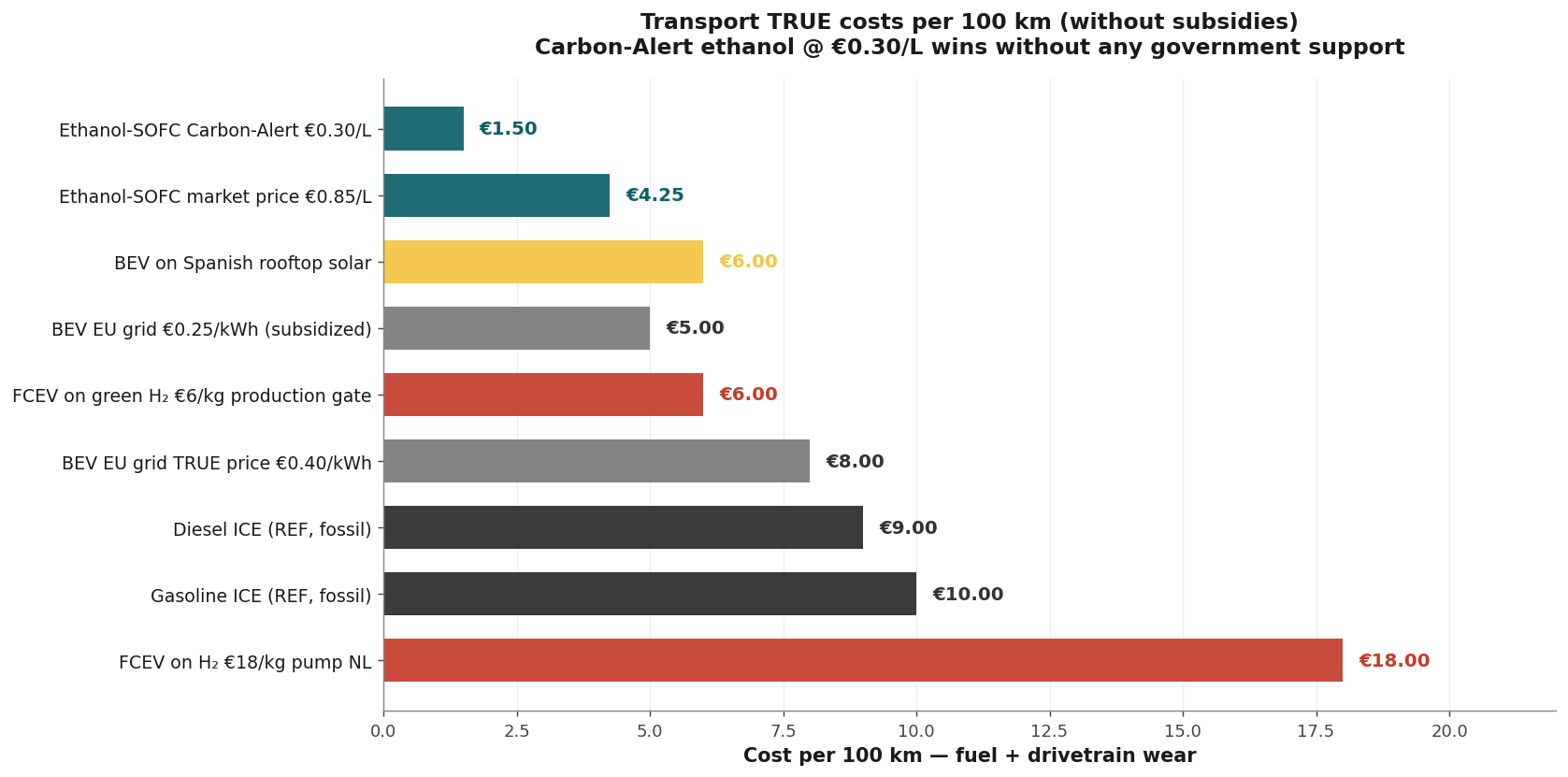

Transport — every drivetrain, every price

A car running ethanol through a SOFC at 78 percent efficiency (Nissan platform, 2036) uses roughly five litres per hundred kilometres. At thirty cents per litre that is €1.50 per hundred kilometres — fuel only. A BEV on rapid charge: €8.50. A hydrogen car at a Dutch pump (€15/kg)3: €15.00. Ethanol-SOFC is per hundred kilometres six to ten times cheaper than its policy-privileged competitors.

Why you hear nothing in Westminster, Berlin, Brussels

The answer is uncomfortable but simple. An entire generation of policymakers has invested personal and political capital in electrification and hydrogen. Subsidy streams, climate agreements, infrastructure plans, and EU packages are built around those two technologies. A third alternative that is demonstrably cheaper and needs no subsidy is not a welcome message. It is a political complication.

The industrial winners are different. Europe's automotive and chemical industries have sunk tens of billions into batteries and hydrogen. Volkswagen, Mercedes, and Stellantis worked within the IPEN framework from 2017 on ethanol fuel cells4. When the political wind shifted to pure electric, they withdrew. Stellantis publicly discontinued hydrogen5. Bosch shut down its SOFC division6. Not for lack of technology. For lack of policy direction. The window closed in Europe while it stands wide open in Japan, Korea, and China.

This is not a conspiracy. It is path dependence — a chain of political and industrial choices from 2015–2025 that reinforced each other and pushed alternatives out of view.

Subsidies accelerated the chosen routes. But they also made them fragile. Without support they collapse. Carbon-Alert is deliberately built differently. It works without.

The bill that isn't on the price tag

A fair comparison also counts external costs. Costs the system produces but that no one sees on the invoice. For electrification and hydrogen, those costs are not small.

- Lithium — clean-up of salt-flat mining in Atacama and Bolivia: €40–€75 per tonne of displaced salt. Water contamination. Conflicts with indigenous communities7.

- Cobalt — Congolese mining with chronic labour abuses, child labour, unclassified mine-collapse disasters.

- Rare earths — China charges €80–€120 per tonne for clean-up of radioactive tailings at Bayan Obo8.

- Battery recycling — European recovery target: 40 percent of lithium, cobalt, nickel. The other 60 percent exits the system as waste.

- Grid expansion for 100 percent electrification — €500–€700 billion EU investment plan to 2040. Borne by the end user through network charges.

The pellet route Carbon-Alert uses has none of these externalities. Residue streams from forestry and agriculture. Local processing. BECCS that removes CO₂ from the air on a net basis. Everything net-negative. Everything in Europe. No mining casualties.

What is needed — today

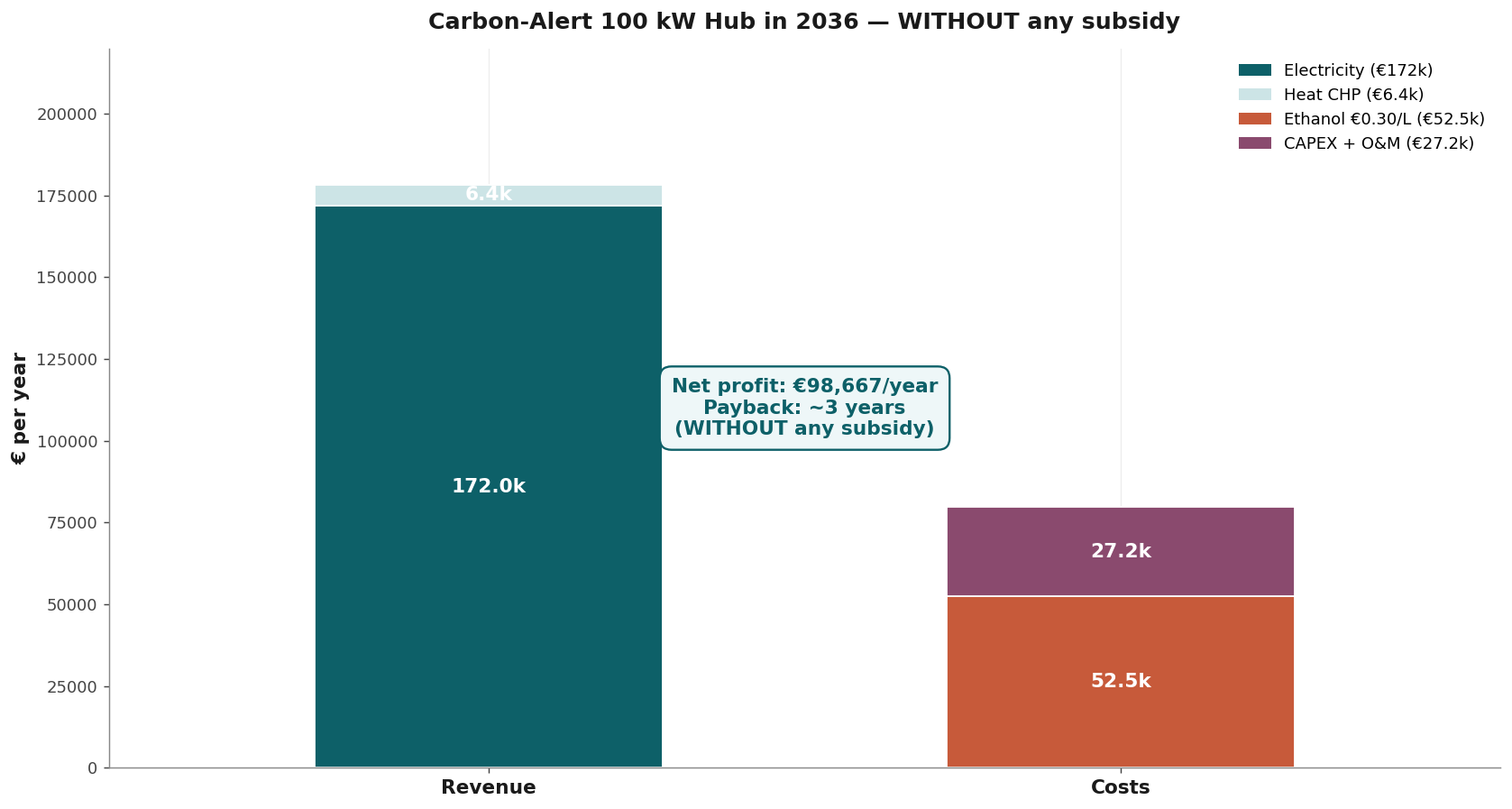

Carbon-Alert Ltd, based in Malta and Mallorca, has worked out the design, documented the learning curves, and calculated the business case without any subsidy. The numbers are clear.

| Indicator | Value | Notes |

|---|---|---|

| Investment 100 kW hub | €180,000 | €1,800/kW SOFC + balance of plant |

| Annual production | 800,000 kWh/year | Capacity factor 91 percent |

| Annual revenue power + CHP | €190,000 | Market prices, no feed-in tariff |

| Fuel + OPEX | −€40,400 | Real ethanol price €0.30/L |

| Net margin year 1 | €59,600 | Rising with scale |

| Payback period | ≈ 3.0 years | Without subsidy |

| Jobs at 50 GW European rollout | 350,000 | Pellet · distillation · SOFC · installation |

| Annual industry revenue | €9 billion | Direct, excluding CO₂ sales |

What government can do — without spending a cent

- Permit acceleration — within six months instead of two to three years for BiCRS and SOFC installations.

- E100 pump standardisation — European standard for a retrofitted petrol station pump.

- Policy neutrality — abolishing the implicit BEV monopoly in zero-emission classifications.

- Education — vocational and technical modules on ethanol operations and SOFC maintenance in 500 European colleges.

- Procurement — public buildings, hospitals, data centres permitted to choose Carbon-Alert hubs without formal barriers.

The question on the table

This article appears in Het Open Vizier because the press in Westminster, Berlin, and Brussels refuses to see these numbers. The question is not whether the technology works. Nissan, Ceres Power, Doosan, Weichai, and Bloom Energy prove it daily. The question is whether Europe still has the courage to follow a technological route that does not lean on subsidies and does not lean on political friends.

What we need is not money. What we need is space.

Space for a technology that works. That is affordable. That creates jobs in disadvantaged regions. That removes CO₂ from the air. That makes Europe less dependent on Chinese rare earths, Congolese cobalt, and Saudi oil.

The thirty cents per litre is not just a price. It is a political choice that becomes irreversible in three years.

Whether Europe makes that choice, we will know by 2030. But the inventors, builders, and investors who make the difference — they are here now. In Mallorca. In Brabant. In Bavaria. In Friesland. In Catalonia. In Lombardy. They ask for no subsidy. They ask for a fair chance in the European market. Before Korea, Japan, and China take that chance away.